Table of Contents

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

Before you even think about picking stocks or opening a brokerage account, you need to get your financial house in order. Seriously. This is the part everyone wants to skip, but it's the bedrock of a successful, stress-free investing journey. Think of it as laying the foundation before you build the skyscraper.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Build Your Financial Foundation Before Investing

Jumping into the market without a solid base is like building a house on sand. It might look fine for a bit, but the first storm that rolls through could bring it all crashing down. That's why the real first step to investing isn't about choosing funds; it's about preparing your finances for the long haul.

Getting this prep work done gives you stability. It means a surprise car repair or an unexpected bill won't force you to cash out your investments at the absolute worst time. When you have this groundwork in place, you can invest with confidence, knowing you have a safety net.

Understand Your Financial Starting Point

You can't plan a road trip without knowing your starting point, right? The same goes for your finances. The first order of business is getting a crystal-clear snapshot of your current financial health, and the best way to do that is with a simple budget.

A budget isn’t about punishment or restriction; it's about awareness. It’s about knowing exactly where your money is going. Just track your income and every single expense for a month. A basic spreadsheet or a budgeting app works perfectly. This little exercise is often an eye-opener, revealing spending habits you never knew you had and freeing up cash you can put toward your goals. Honing your money management skills is the single most important thing you can do for your financial future.

Once you know the numbers, you can start mapping out a path forward. That clarity is everything.

Create a Financial Safety Net

One of the biggest mistakes new investors make is having to sell their investments to cover an emergency. To avoid this trap, you need an emergency fund. This is just a boring old savings account with enough cash to cover 3 to 6 months of your essential living expenses.

Your emergency fund isn't an investment; it's your financial insurance policy. It's what protects your actual investments from life's curveballs, allowing them to grow without interruption.

Let's say your non-negotiable monthly bills (rent, utilities, food, transport) add up to £2,000. Your goal for this fund should be somewhere between £6,000 and £12,000, stashed away in an easy-to-access, high-yield savings account. Don't be intimidated by the final number—start small. Set up an automatic transfer of just £50 each payday. The momentum will build faster than you think.

Prioritize High-Interest Debt Repayment

High-interest debt is the arch-nemesis of building wealth. I'm talking about credit cards, payday loans, and anything else with an interest rate that makes your eyes water. With rates often north of 20% annually, this kind of debt will sabotage your investment returns before you even get started. The stock market might give you an average return of 8-10% over the long run, but your credit card debt is costing you double that.

Think about it this way: paying off a credit card with a 22% APR is the same as getting a guaranteed, tax-free 22% return on your money. You will not find that kind of guaranteed return anywhere else.

Here’s a simple game plan to tackle it:

- List Your Debts: Get it all down on paper. Every debt, its current balance, and its interest rate.

- Target the Highest Rate: Funnel every spare penny you have toward the debt with the highest interest rate while just making the minimum payments on everything else. This is the "avalanche method," and it's the fastest way to get out of debt mathematically.

- Automate Everything: Set up automatic payments so you're consistent and never miss a due date.

Once you have a budget, an emergency fund, and a plan for your high-interest debt, you've built a solid launchpad. This foundation doesn't just get you ready to invest; it sets you up for long-term success.

Choose the Right Investment Account for You

So, you’ve got your budget in order, an emergency fund ready, and you're tackling any high-interest debt. Fantastic. Now for the exciting part: choosing where to actually put your money to work.

Think of an investment account as the "house" where your investments (like stocks, bonds, and funds) will live. The type of house you pick has a huge impact on your taxes, how easily you can access your money, and how fast your wealth can grow. Your choice really comes down to your goals. Are you playing the long game for retirement, or are you saving for something closer on the horizon, like a down payment on a house in five years?

Differentiating Your Account Options

The world of investing can seem like a confusing alphabet soup of accounts, but for most people starting out, it really boils down to three main choices. Each one is built for a different purpose, especially when it comes to taxes and when you’ll need to pull the money out. Getting this right from the start is one of the easiest ways to make sure your money is working as hard as possible for you.

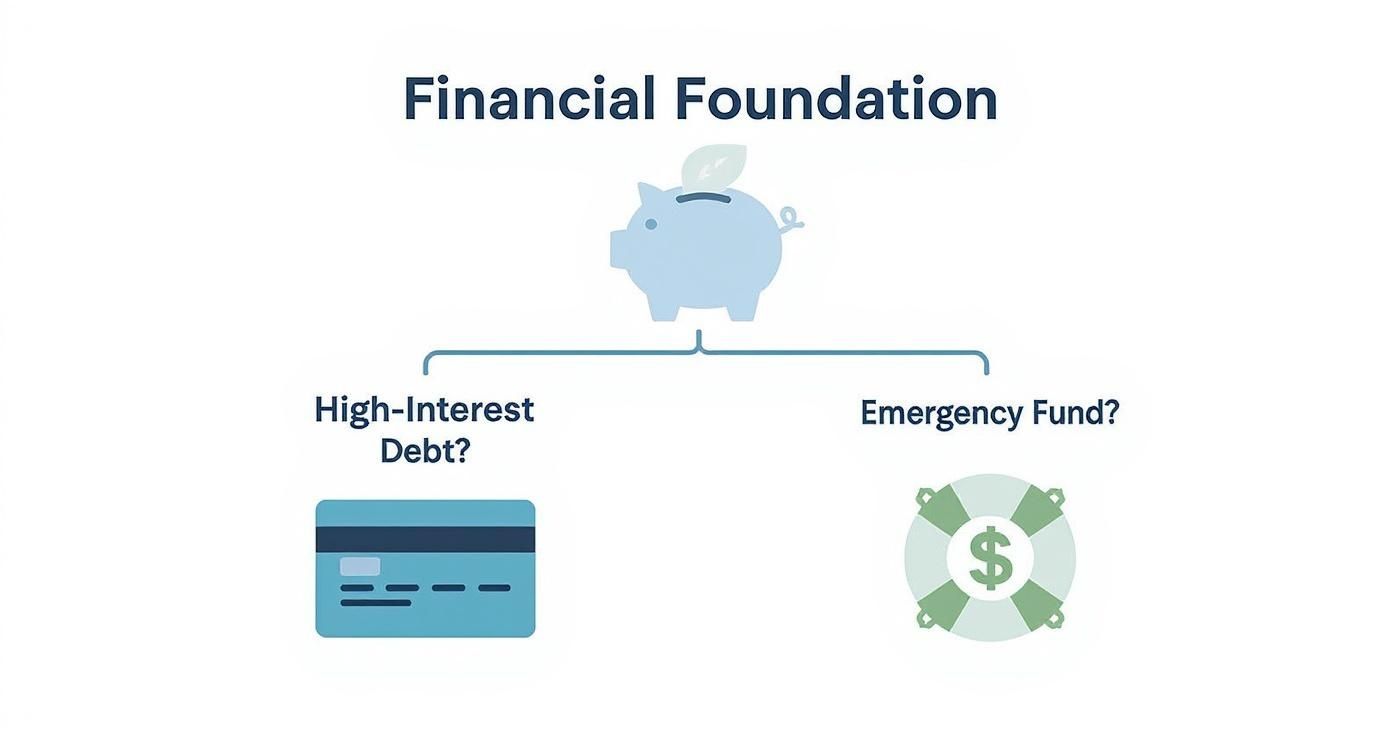

Before we get into the nitty-gritty, this chart lays out how a solid financial base sets you up for success.

It’s a great visual reminder that you want to be investing from a position of strength, not desperation. With that foundation in place, let's compare the accounts.

To make sense of the main options, it helps to see them side-by-side. Each has its own strengths depending on what you're trying to accomplish.

Comparing Beginner Investment Accounts

| Account Type | Primary Purpose | Tax Advantage | Key Benefit for Beginners |

|---|---|---|---|

| Standard Brokerage | General investing for non-retirement goals | None (taxable) | Maximum flexibility; withdraw funds anytime for any reason. |

| Roth IRA | Retirement savings | Tax-free growth and withdrawals | Your money grows and can be taken out in retirement completely tax-free. |

| Traditional IRA | Retirement savings | Tax-deferred growth; possible upfront tax deduction | Contributions might lower your taxable income today. |

| 401(k) | Retirement savings (through an employer) | Tax-deferred growth; possible upfront tax deduction | The potential for an employer match is "free money." |

Ultimately, you might end up using a combination of these accounts over your lifetime. The key is to start with the one that best aligns with your immediate priorities.

The Standard Brokerage Account: Flexibility First

A standard brokerage account, sometimes called a "taxable brokerage account," is your all-purpose investing tool. You open one with a firm like Fidelity or Vanguard, deposit cash, and you're free to buy whatever you want—ETFs, index funds, you name it.

There are no limits on how much you can contribute, and you can pull your money out whenever you want without penalty. This makes it the go-to choice for goals that aren't decades away. Saving for a wedding in three years or a car in five? A brokerage account gives you that freedom. The catch? It has no special tax perks. You'll owe capital gains taxes on any profits when you sell investments.

Retirement Accounts: Tax-Advantaged Growth

This is where things get really powerful for long-term wealth building. Retirement accounts are designed specifically for your golden years, and the government gives you some pretty sweet tax breaks as an incentive to use them. For individuals, the two most common types are the Traditional and Roth IRAs (Individual Retirement Accounts).

-

Traditional IRA: Your contributions might be tax-deductible, which is a great way to lower your tax bill today. Your money then grows tax-deferred, meaning you don't pay any taxes on it until you withdraw it in retirement.

-

Roth IRA: This is a favorite for many beginners, and for good reason. You contribute with after-tax dollars (so no upfront deduction), but your investments grow completely tax-free. When you take the money out in retirement, it's all yours, with no tax bill attached.

For a lot of people just starting their careers, the Roth IRA is a brilliant move. You pay the taxes now while your income (and tax bracket) is likely lower than it will be in the future.

Employer-Sponsored Plans: The Power of the Match

If your job offers a retirement plan like a 401(k) or 403(b), this should be your first stop. Seriously. It’s a fantastic tool on its own, but its killer feature is the employer match.

Many companies will match your contributions up to a certain percentage of your salary. This is free money. It's an immediate, guaranteed 100% return on your investment that you simply cannot get anywhere else. Turning down a full company match is like refusing a raise.

For example, if your company matches 100% of your contributions up to 4% of your salary, your absolute minimum goal should be to contribute 4% of your pay. Once you’ve secured that full match, you can then look at putting any extra savings into an IRA to get more investment options and tax diversification.

Understand Your First Investment Options

Alright, you've got your accounts open and ready to go. Now for the million-dollar question: what do you actually buy? The wall of options can feel intimidating, but the secret for new investors is to tune out the noise. Forget about trying to find the next Apple or Tesla.

Seriously. The best move you can make right now is to ditch the idea of picking individual stocks. A much smarter—and historically more effective—approach is to simply buy a tiny piece of the entire market. This sounds complicated, but modern investment products make it incredibly easy to do.

The Magic of Index Funds and ETFs

Imagine owning a small slice of hundreds of the biggest, most successful companies in America with a single click. That's exactly what index funds and Exchange-Traded Funds (ETFs) let you do. They are the essential building blocks for any sensible beginner's portfolio.

-

Index Funds: Think of these as a basket that holds all the stocks from a specific market index, like the S&P 500. Instead of a manager trying to pick winners, the fund just buys everything in the index it’s designed to follow. It’s a passive, hands-off approach.

-

ETFs (Exchange-Traded Funds): These are a lot like index funds—they also hold a basket of stocks that track an index. The main difference is that you can buy and sell them throughout the day like a regular stock, so their price can tick up and down from minute to minute.

For a beginner, the difference between the two is pretty minor. Both give you incredible diversification for a very low cost, which is the perfect combination when you're just starting out.

A Real-World Example: The S&P 500

Let's make this concrete by looking at the most famous index of all: the S&P 500. This index is simply a list of the 500 largest public companies in the U.S. When you buy an S&P 500 index fund or ETF, you instantly become a part-owner in giants like Apple, Microsoft, Amazon, and hundreds of others.

This chart shows you all the different business sectors that make up the S&P 500.

As you can see, buying just this one fund spreads your money across everything from Information Technology to Health Care. Your risk is automatically spread out. If one company or even an entire industry has a bad year, the other 499+ companies in the fund help soften the blow. It’s the classic "don't put all your eggs in one basket" strategy, automated for you.

This accessibility has completely changed the game. It’s never been easier for everyday people to start building wealth. In fact, over 58% of U.S. households now own investments, a big jump from just 49% in 2010. With the rise of fractional shares, you can get started with as little as $1. To learn more, check out this guide to the major asset classes available to beginners.

Don't Forget About Bonds

While stock funds are the engine for growth in your portfolio, bonds play a totally different—and equally crucial—role: they provide stability.

Think of stocks as the accelerator in your car and bonds as the brakes. You need both. The gas pedal gets you to your destination, but the brakes keep you safe and in control when the road gets bumpy.

So, what is a bond? It's basically a loan you make to a government or a big corporation. In exchange for your money, they promise to pay you regular interest for a set amount of time. When that time is up, you get your original investment back.

Bonds are generally much less risky than stocks. When the stock market gets choppy or takes a dive, bonds often hold their value or even increase a bit. Having a slice of your portfolio in a bond ETF or index fund acts as a shock absorber, giving you the peace of mind to stick with your plan instead of panic-selling.

Construct Your First Investment Portfolio

Alright, you've got the lay of the land—you know about the different accounts and what you can put inside them. Now for the fun part: actually putting it all together. Building your first portfolio isn't about trying to find the next big stock market winner. It’s more like creating a recipe that’s perfectly suited to your financial goals and how long you plan to invest.

The single most important decision you'll make right now is your asset allocation. That’s just a fancy term for how you split your money between different kinds of investments—mostly, stocks and bonds. This mix is the real driver of your long-term returns and will determine just how bumpy the ride is.

Finding Your Ideal Asset Mix

Your perfect mix really boils down to two key things: your time horizon (when you'll need the cash) and your risk tolerance (how you stomach market ups and downs). If you're young with decades to go until retirement, you can generally afford to take on more risk for the chance at higher growth. But if you’re getting closer to your goal, you’ll probably want a bit more stability.

Here’s a simple way to think about it:

- Stocks (ETFs/Index Funds): These are your portfolio's growth engine. They offer the highest potential returns but also come with more volatility.

- Bonds (ETFs/Index Funds): Think of these as your portfolio's shock absorbers. They provide stability and income, but usually with lower returns and less risk.

This balance is deeply personal, but there are a few tried-and-true models that are perfect for beginners. These simple "two-fund" portfolios are a breeze to set up and manage using low-cost ETFs.

Here are a few common starting points based on different comfort levels with risk:

-

Aggressive Growth (High Risk Tolerance):

- 90% in a total stock market ETF (like one that tracks the S&P 500 or a global index).

- 10% in a total bond market ETF.

- This is a great fit for someone in their 20s or early 30s who has plenty of time to ride out market fluctuations.

-

Moderate Growth (Medium Risk Tolerance):

- 70% in a total stock market ETF.

- 30% in a total bond market ETF.

- This allocation strikes a nice balance between solid growth potential and a smoother ride.

-

Conservative Growth (Low Risk Tolerance):

- 60% in a total stock market ETF.

- 40% in a total bond market ETF.

- This classic 60/40 split is designed to dampen market swings and might be right for someone who’s more risk-averse or has a shorter timeframe.

The beauty here is in the simplicity. You don't need a dozen funds to be properly diversified. A single broad stock market ETF and one bond market ETF can give you a slice of thousands of companies and bonds from all over the world.

The Power of Consistent Investing

Once you’ve picked your mix, the real secret to success isn't some complex trading strategy. It’s a boring, disciplined habit: investing consistently, month after month, no matter what the market is doing. This is where a powerful technique called Dollar-Cost Averaging (DCA) becomes your best friend.

DCA just means investing a fixed amount of money at regular intervals—say, £100 every month. It’s an incredibly smart move for beginners because it takes emotion completely out of the picture. You're not trying to "time the market" by guessing when prices are low. You just invest methodically.

By investing the same amount each month, you automatically buy more shares when prices are low and fewer shares when prices are high. This can lower your average cost per share over time and turn market volatility into your friend.

This simple, automated approach removes all the anxiety of trying to figure out the "perfect" time to jump in. The best time to invest is whenever you have the money, and DCA makes that happen seamlessly.

This isn't just theory; it works. Historical data shows that over the past 20 years, investors who simply used DCA to invest in the S&P 500 index saw an average annual return of about 8.5%. If you're interested in digging deeper, you can discover more insights about long-term investment trends on Mintos.com.

Putting It All Together: A Practical Example

Let's walk through how this looks in the real world for a beginner investor named Alex.

- Goal: Long-term retirement savings.

- Age: 28 years old.

- Risk Tolerance: Moderate to high.

- Monthly Investment: £200.

Following the game plan we've laid out, Alex decides on a portfolio of 80% stocks and 20% bonds. He hops onto his brokerage account and sets up an automatic transfer and investment plan.

Now, every single month, his £200 gets put to work automatically:

- £160 buys shares of a low-cost S&P 500 ETF.

- £40 buys shares of a low-cost total bond market ETF.

Alex doesn’t check the market every day. He doesn't panic when the news cycle gets crazy. He just lets the automation do its thing, trusting in the power of dollar-cost averaging and the long-term growth of his diversified portfolio. This simple, disciplined strategy is exactly how beginners start investing and build real, lasting wealth.

Common Investing Mistakes and How to Sidestep Them

Alright, we've covered the "what to do" part of building your first investment portfolio. Now it’s time for something just as important: what not to do. Getting this right from the start can save you a ton of money and stress down the road.

Frankly, the biggest hurdles for new investors aren't complex financial models; they're the mental traps we all fall into. The market runs on data, but human emotions like fear and greed are always in the driver's seat. Learning to manage your own reactions is one of the most powerful skills you can develop.

Don't Try to Time the Market

This is the big one. Everyone fantasizes about being the genius who sells at the absolute peak and buys at the very bottom. It’s a tempting idea, but trying to time the market is a fool's errand. Even the pros with supercomputers can't do it consistently.

Market highs and lows are only ever crystal clear in hindsight. What often happens is that the market's best days come hot on the heels of its worst days. If you jump out in fear, you’ll likely miss the powerful rebound that follows.

The numbers don't lie. A J.P. Morgan Asset Management study looked at the S&P 500 from 2003 to 2022. Staying invested the whole time would have earned you a 9.8% annual return. But if you missed just the 10 best days over those two decades? Your return would have tanked to 5.5%.

Forget being a market psychic. The real key is time in the market, not timing the market. Set up a consistent, automated investment plan and let it do the heavy lifting for you.

Don't Let Your Emotions Drive

Turn on any financial news channel, and you'll be bombarded with drama. Every little dip is a "CRASH," and every uptick is a "SURGE." This constant hype is designed to get a reaction, and it often leads beginners into two classic blunders:

- Panic Selling: The market drops, and your stomach sinks with it. The urge to sell everything to "stop the bleeding" is overwhelming. But selling in a downturn just locks in your losses and guarantees you won't be around for the recovery.

- Performance Chasing: This is driven by pure FOMO (fear of missing out). You see a stock or fund that's gone to the moon and pile in, hoping to catch the ride. More often than not, you end up buying high, right before gravity takes over.

The best defense is a good offense. Create your investment plan when you're calm and rational. Then, when things get choppy, stick to it. Tune out the noise and trust the process you built.

Don't Ignore the Fees

Investment fees look tiny on paper—just a fraction of a percent. But they are silent portfolio killers. Over decades, the power of compounding works against you, turning small fees into a massive drag on your returns.

Let’s look at a simple example. You invest £10,000 and let it grow for 30 years with a 7% average annual return.

| Expense Ratio | Fees Paid Over 30 Years | Final Portfolio Value |

|---|---|---|

| 0.04% | £966 | £75,283 |

| 1.04% | £18,040 | £58,209 |

That seemingly insignificant 1% difference in fees devoured over £17,000 of your potential returns. It’s a huge deal.

Always, always choose low-cost index funds and ETFs. I personally look for funds with expense ratios well under 0.20%. The money you save on fees compounds into real wealth over time.

Don't Over-Complicate Things

Diversification is essential, but it’s easy to go overboard. Some new investors think owning 50 different funds makes them safer. In reality, it just creates over-diversification.

You end up with a portfolio full of overlapping assets that basically just mimics the entire market anyway. The only difference is that your version is more complex and probably comes with higher fees.

For most people starting out, simple is better. A solid portfolio built from just two or three broad, low-cost funds—think a total US stock fund, a total international stock fund, and a total bond fund—gives you all the diversification you need without the headache.

Got Questions About Investing? We've Got Answers

Diving into the world of investing is exciting, but let's be real—it also brings up a ton of questions. Getting straight answers is the best way to build the confidence you need to get started. Here’s a rundown of the most common things beginners ask.

How Much Money Do I Actually Need to Start?

You can get started with a lot less cash than you probably think. Seriously. The old days of needing thousands of pounds just to open an account are long gone.

Today, with so many brokerage platforms offering no minimum deposits and the magic of fractional shares, you can literally start with £5 or £10. The real key isn't how much you start with; it's about building the habit of investing consistently. Starting small with automatic, regular deposits is way more powerful than waiting to save up a huge lump sum.

Is the Stock Market Just a Big Casino? Is It Safe?

Look, every investment has some risk. It’s true that the value of your portfolio can go down. But risk isn't something you just have to accept—it's something you can manage.

Instead of trying to hit a home run by picking individual stocks (which is incredibly difficult), you can spread your risk instantly by using diversified, low-cost index funds or ETFs. This means your money is invested across hundreds, or even thousands, of different companies. If one company tanks, it doesn't sink your whole portfolio.

While the market has its ups and downs day-to-day, history has shown it consistently trends upward over the long haul, rewarding investors who don't panic and simply stay the course.

How Often Should I Be Checking My Investments?

This might sound counterintuitive, but for long-term investors, checking your portfolio constantly is one of the worst things you can do. It's a recipe for anxiety and can lead you to make emotional decisions based on perfectly normal market swings.

Seeing a temporary dip can make you feel like you need to do something right away, when the best move is usually to do nothing at all.

A much healthier approach is to check in once a quarter or maybe twice a year. That’s often enough to see if you need to rebalance, but not so often that you get caught up in the daily noise.

Keep your eyes on the long-term prize. The small savings you make in other areas of your finances can be put to better use in your investment account without you needing to obsess over its daily performance.

What’s the Real Difference Between an ETF and an Index Fund?

For a beginner, they both serve the same fantastic purpose: giving you instant diversification at a very low cost. The main difference is simply how they're bought and sold.

- ETFs (Exchange-Traded Funds): These trade on a stock exchange, just like a regular stock. Their price can change throughout the day as people buy and sell them.

- Index Funds: These are a type of mutual fund. They only have one price per day, which is calculated after the market closes.

ETFs sometimes have slightly lower fees and can be a bit more tax-efficient in a regular brokerage account. But honestly, for a beginner building a portfolio for the long haul, either one is an excellent choice for tracking a market index and capturing its returns.

At Collapsed Wallet, our goal is to give you the clear, practical guidance you need to take control of your money and build a secure future. Explore more of our guides and tools to continue your journey toward financial freedom. Visit us at https://collapsedwallet.com.

8 thoughts on “How to Start Investing for Beginners: A Quick Guide”