Table of Contents

- Giving Every Pound a Purpose with Zero-Based Budgeting

- The “Start from Scratch” Philosophy

- How ZBB Compares to Other Budgeting Methods

- The Real Pros and Cons of a Zero-Based Budget

- Your Step-by-Step Guide to Creating a Zero-Based Budget

- Common Pitfalls and How to Make ZBB Work for You

- Common Questions About Zero-Based Budgeting

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

Ever get to the end of the month and wonder where all your money went? You had a plan, you thought you were being careful, but somehow, cash just seems to evaporate. It’s a classic problem, and it’s exactly what zero based budgeting is designed to fix.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Put simply, zero-based budgeting is a method where every single pound you earn gets a specific job. From bills and essential spending to savings and investments, everything is accounted for. The goal is simple: income minus expenses must equal zero. This isn’t about being restrictive; it’s about being deliberate with your money so it actually works toward your financial freedom.

Giving Every Pound a Purpose with Zero-Based Budgeting

Most of us budget by looking at last month’s spending and tweaking it a little. The trouble is, this often means old, wasteful habits and forgotten subscriptions just roll over from one month to the next without a second thought. Zero-based budgeting completely flips that script.

Instead of adjusting last month’s numbers, you start from scratch. Every single time. This forces you to justify every expense, asking not just “Can I afford this?” but “Is this expense truly important for achieving my financial goals right now?”

The Core Principle Explained

At its heart, zero-based budgeting boils down to a simple formula: Income – Expenses = £0. This doesn’t mean you need to drain your bank account by the end of the month. It means every pound that comes in is consciously assigned to a category.

You’re essentially pre-spending your entire income on paper (or a spreadsheet). This includes:

- Essential Bills: Mortgage/rent, utilities, council tax—the non-negotiables.

- Variable Spending: Groceries, fuel, and other costs that fluctuate.

- Savings Goals: Your emergency fund, retirement pot, or a deposit for a house.

- Debt Repayment: Chipping away at loans or credit cards.

- Personal Spending: Money for hobbies, entertainment, and personal well-being.

By giving every pound a home, you eliminate that black hole where money seems to disappear. Your budget stops being a backward-looking report and becomes a forward-looking plan. Of course, making a plan is one thing; sticking to it is another. If you struggle with that, we have a guide on how to create a budget you will stick to.

This method transforms your mindset from passively tracking money to actively directing it toward what matters most to you. It’s about being the CEO of your own finances.

Why Intentionality Matters

Think of your income as a team of employees. With a typical budget, some are working hard (paying bills), but others might be wandering around aimlessly (random, untracked spending). In a zero-based budget, you’re the manager assigning a specific, crucial task to every single employee.

This intense focus forces you to look your spending habits right in the eye. You’ll quickly spot where your money is aligned with your values and—more importantly—where it isn’t. At its core, zero-based budgeting is a powerful approach to resource optimization, making sure every penny is used as effectively as possible. It’s perfect for anyone who feels like their finances are controlling them, not the other way around.

The “Start from Scratch” Philosophy

Think of it this way: traditional budgeting is like renovating an old house. You work with the existing structure, maybe patching a few holes or adding a fresh coat of paint, but you’re fundamentally stuck with the original layout. Old habits, forgotten subscriptions, and wasteful spending often get carried over from one month to the next without a second thought.

Zero-based budgeting (ZBB) is completely different. It’s like starting with a blank blueprint for a brand-new home. You decide where every single wall, window, and door goes based on what you actually need right now. Nothing is assumed.

By starting from zero each month, this method forces you to justify every expense. It flips your perspective from passively tracking where your money went to actively deciding where it will go.

A Mindset of Intentional Spending

The entire philosophy of ZBB boils down to one word: intentionality. This isn’t about being restrictive; it’s about making conscious choices that line up with what you truly value. Every pound is given a specific job, a clear purpose that moves you closer to your financial goals.

To successfully build this kind of budget, a solid grasp of understanding income and expenses is your essential starting point. It’s the foundation for everything that follows.

This approach makes you ask tougher, more meaningful questions. Instead of simply asking, “How much did I spend on groceries last month?” you start asking, “How much do I need to spend on groceries this month to stay healthy and on track with my savings goals?”

Zero-based budgeting turns your budget from a historical record of past mistakes into a forward-looking roadmap for future success. It’s about building the financial life you want, not just maintaining the one you have.

From the Boardroom to Your Kitchen Table

This idea of starting from a blank slate actually comes from the corporate world. It was developed back in the 1970s by a manager named Peter Pyhrr who saw a major flaw in how companies handled their finances. He argued that the common practice of just adding a small percentage to last year’s budget—known as incremental budgeting—was a recipe for bloated, inefficient spending.

His solution was radical for its time: make every department build its budget from the ground up, justifying every single cost as if it were a brand-new initiative. This process ensured money only went to the most critical and valuable activities, a principle that works just as brilliantly for our personal finances.

How It Powers Your Personal Goals

Bringing this strategy home can be incredibly powerful. It forces you to draw a direct line from every pound you spend to a personal goal or value.

Here’s why this “start from scratch” philosophy works so well:

- It Exposes Waste: It shines a bright light on non-essential spending. You’ll immediately spot that gym membership you never use or the three streaming services you forgot you were paying for.

- It Encourages Adaptability: Life is unpredictable. If your income changes or a new priority pops up, your budget can pivot right along with you. It’s built to be flexible, not rigid.

- It Builds Financial Confidence: Making deliberate choices puts you firmly in the driver’s seat. This feeling of control is a huge step in reducing money-related stress and building momentum toward your biggest goals.

Ultimately, this budgeting philosophy is about empowerment. It’s a powerful declaration that you are in charge, building the future you want one intentional pound at a time.

How ZBB Compares to Other Budgeting Methods

Picking a budgeting method is a lot like choosing the right tool for a home improvement project. You wouldn’t use a sledgehammer to hang a picture frame, right? To really see where zero-based budgeting (ZBB) fits into your financial toolkit, it helps to put it side-by-side with other popular systems.

While every method is designed to help you get a handle on your money, they work in fundamentally different ways. Some are all about simplicity and getting started quickly, while others—like ZBB—demand a much more hands-on, detailed approach. Finding the one that clicks with your personality, lifestyle, and financial goals is the key to success.

Traditional Budgeting: The Path of Least Resistance

Most people fall into traditional budgeting without even thinking about it. The process is simple: take last month’s spending, make a few small adjustments for anything new, and call it a day. If you spent £300 on groceries in June, you’ll probably budget £300 for July.

The main draw here is speed. It’s easy. But that convenience has a hidden cost. Traditional budgeting is notorious for letting wasteful habits and long-forgotten subscriptions roll over month after month, completely unchallenged. It’s more about maintaining your current financial situation than actively trying to improve it.

The 50/30/20 Rule: Simplicity for Beginners

The 50/30/20 rule has become incredibly popular because it’s so easy to grasp. It’s a percentage-based budget that splits your after-tax income into three simple buckets:

- 50% for Needs: This is for all your absolute essentials—rent or mortgage, utilities, transportation, and groceries.

- 30% for Wants: This bucket covers the fun stuff, like dining out, hobbies, streaming services, and shopping.

- 20% for Savings and Debt Repayment: This is where you build your future, whether that’s saving for a down payment, investing, or crushing your credit card debt.

This method gives you a fantastic high-level framework without getting lost in the weeds. Its biggest weakness, though, is that it doesn’t push you to question the individual expenses hiding within those big categories.

Envelope Budgeting: The Tangible Cash Method

For anyone who works better with something they can touch and feel, the envelope system is a time-tested classic. You literally withdraw cash for different spending categories (like ‘Groceries’ or ‘Petrol’) and put it into labeled envelopes. When an envelope is empty, you’re done spending in that category for the month. Simple as that.

This method is brilliant for reining in overspending because it makes your budget physically real. The main challenge, of course, is that it’s built around cash in an increasingly digital world. It’s not great for handling online bills or subscriptions.

Zero-based budgeting really stands out because it blends the intense detail of the envelope method with the flexibility needed for modern, digital banking. It doesn’t just track where your money went; it forces you to justify where every single pound is going.

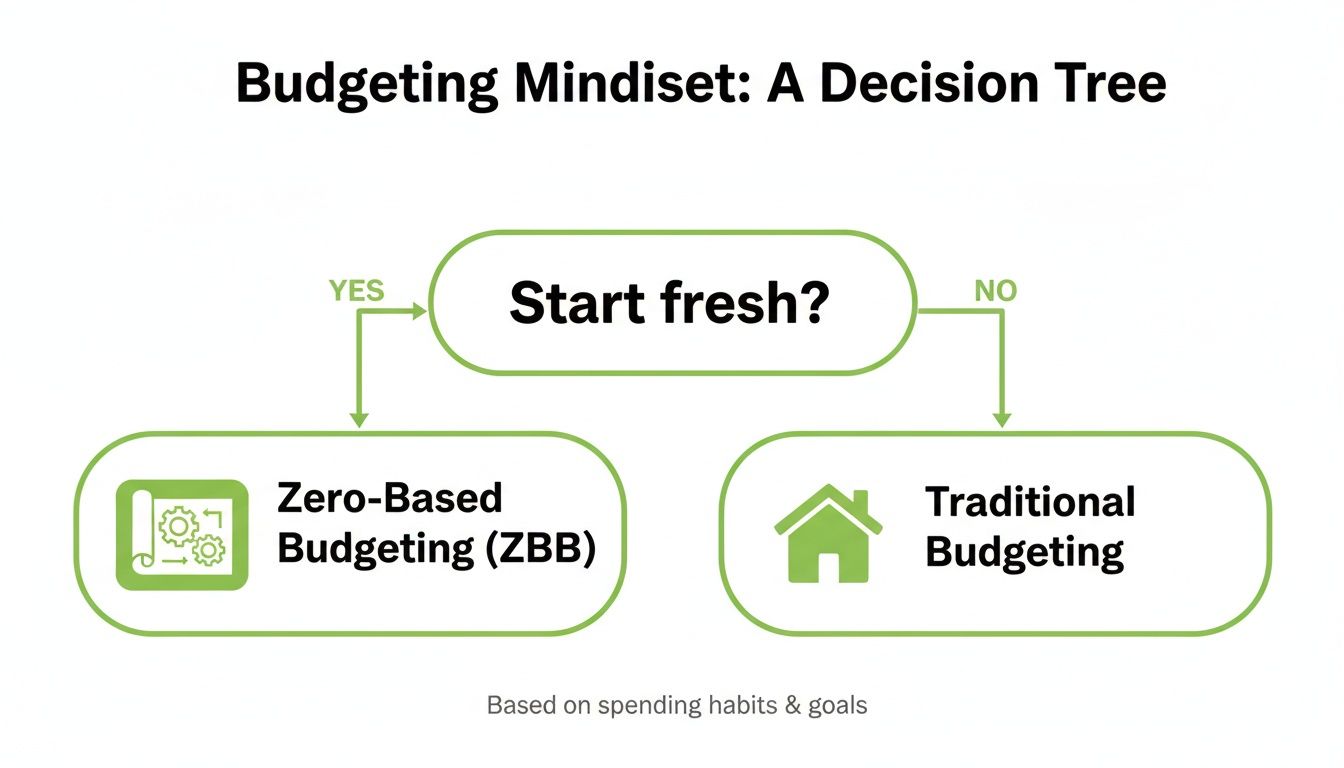

Why ZBB Is Different

This decision tree visualizes the core difference in mindset between ZBB and more traditional approaches.

The image gets to the heart of the matter: do you want to build your budget from scratch every single month (the ZBB way), or just tweak last month’s plan?

A Quick Comparison of Budgeting Methods

To make it even clearer, let’s break down how these methods stack up against each other. Each has its place, but they serve very different needs.

| Budgeting Method | Core Principle | Best For | Key Drawback |

|---|---|---|---|

| Zero-Based Budgeting | Every pound has a job. Income minus expenses equals zero. | Detail-oriented people, those with irregular income, or anyone serious about cutting costs. | Time-consuming and requires significant monthly effort. |

| Traditional Budgeting | Use last month's budget as a baseline and adjust slightly. | People with stable incomes and predictable expenses looking for a quick method. | Can lead to lifestyle creep and lets wasteful spending go unnoticed. |

| 50/30/20 Rule | Allocate income into three fixed percentages: Needs, Wants, and Savings. | Beginners who want a simple, high-level guide without tracking every penny. | Lacks detail; "Needs" vs. "Wants" can be too subjective or restrictive. |

| Envelope Budgeting | Use physical cash in envelopes to control spending in variable categories. | Visual, hands-on budgeters who struggle with overspending on things like food or entertainment. | Impractical for online purchases, bills, and a cashless society. |

Ultimately, ZBB is the most intentional and meticulous of the bunch. While the 50/30/20 rule gives you guardrails and the envelope system puts a physical limit on cash spending, ZBB demands that you actively and consciously build a brand-new plan from the ground up, every single time. It’s more work, no doubt. But the reward is a budget that’s perfectly tuned to your current reality and laser-focused on your future goals.

The Real Pros and Cons of a Zero-Based Budget

Switching to a zero-based budget feels like hitting the reset button on your finances. But before you dive in, it’s smart to look at both sides of the coin. Like any method, it has some powerful benefits but also a few potential headaches. Knowing what you’re getting into is the key to deciding if this hands-on approach is the right one for your financial journey.

The biggest win? Unmatched financial clarity. You’re building your budget from the ground up every single month, which gives you a ridiculously clear picture of where every pound is going. This process forces you to consciously connect your spending to your goals, making it way easier to spot and cut out wasteful habits.

The Clear Advantages of Adopting ZBB

This method is so much more than a simple tracking system—it’s a game plan for your money. And the best part is that its benefits tend to build on each other over time, leading to some serious financial progress.

Here’s a breakdown of the main upsides:

- Optimised Spending: ZBB makes you justify every expense, not just new ones. This puts a spotlight on “budget bloat”—think forgotten subscriptions or mindless spending habits—and helps you redirect that cash toward things that actually matter to you.

- Enhanced Goal Alignment: Every single pound gets a specific job to do, whether it’s crushing debt, saving for a holiday, or building your investment portfolio. Your budget stops being a list of rules and becomes an active tool for building the life you want.

- Greater Accountability: When you build the plan yourself from scratch, you feel a real sense of ownership. That personal investment makes it much easier to stick to your guns and say no to impulse buys that aren’t part of the plan.

- Flexibility for Variable Incomes: If you’re a freelancer, gig worker, or have an income that bounces around, ZBB is a lifesaver. It lets you create a fresh plan based on the actual money you have this month, instead of trying to force a fixed budget to work when your earnings are all over the place.

The real power of a zero-based budget is its intentionality. It shifts your mindset from just watching your money disappear to actively telling it where to go. You’re in the driver’s seat.

This isn’t just theory, either. ZBB saw a huge resurgence after the 2008 recession as companies and families alike got serious about their finances. In fact, a 2022 survey from a budgeting app built on these principles found that users who gave every pound a job saved 15% more each month. What’s more, families using this approach cut their debt by an average of 23% in just one year. You can read more about these findings and see how businesses have even trimmed costs by 12% using ZBB.

The Potential Downsides to Consider

While the benefits are compelling, it’s not all sunshine and rainbows. It’s important to be honest about the challenges. Ignoring them can lead to frustration and burnout, which might make you quit before you even start seeing the results.

The most common complaint is the initial time commitment. That first month with a zero-based budget is going to be intense. You have to track down every income source and list out every single expense, which can feel a bit overwhelming at first.

Here are the main cons to keep in mind:

- It Can Be Time-Consuming: Especially when you’re starting out, creating a brand-new budget each month takes real time and focus. It gets faster with practice, but it’s definitely not a “set it and forget it” system.

- Risk of Getting Lost in the Details: It’s easy to get so caught up in accounting for every last penny that you lose sight of the big picture. The goal is to control your money, not to let the tiny details of budgeting control you.

- Potential for Short-Term Focus: Because you’re resetting the budget every month, there’s a risk of focusing too much on immediate costs. You have to be deliberate about making sure long-term goals, like retirement or investments, don’t get pushed aside.

- Can Feel Restrictive: For some people, the idea of giving every pound a job feels suffocating. If you prefer a more laid-back, hands-off approach to your money, the detailed nature of ZBB might feel more like a chore than a path to freedom.

Ultimately, deciding if what is zero based budgeting is right for you comes down to a simple trade-off. Are you willing to put in more time and effort upfront in exchange for total control and clarity over your finances? For anyone serious about hitting their financial goals, the answer is often a definite “yes.”

Your Step-by-Step Guide to Creating a Zero-Based Budget

Ready to roll up your sleeves and build your first zero-based budget? I know it can sound a bit intense, but it’s really just a logical process that gives you incredible clarity over where your money is going. If you break it down into manageable chunks, what seems like a huge task quickly becomes an empowering monthly routine.

This guide walks you through the five essential steps to craft a budget where every single pound has a purpose. We’ll start with the money coming in and finish with a rock-solid plan you can put into action right away.

Step 1: Calculate Your Total Monthly Income

First things first: before you can tell your money where to go, you need to know exactly how much you have. This figure is the bedrock of your entire budget. For most people with a steady salary, this is pretty straightforward.

Pull together all your sources of income for the month after taxes and deductions have been taken out. This means looking at:

- Your main salary: The amount that actually lands in your bank account from your primary job.

- Side hustle money: Anything you earn from freelancing, a part-time gig, or any other side projects.

- Other income sources: This could be anything from benefits and rental income to dividends from investments.

Add it all up. That final number is your starting line—it’s the total amount of cash you have to work with for the month.

Now, if your income fluctuates, the approach is a little different. Instead of guessing or using an average, it’s much safer to build your budget around your lowest expected monthly income. This gives you a reliable baseline to work from. Any extra cash you earn above that amount can then be assigned to a specific goal—like smashing a debt or boosting your emergency fund—as soon as it comes in.

Step 2: List Every Single Expense

Here’s where the real work—and the real insight—begins. Your mission is to track down and list everything you spend money on in a typical month. And I mean everything. Don’t leave out that morning coffee or the odd magazine purchase.

The easiest way to do this is to grab your bank and credit card statements from the last two to three months. Go through them line by line and start categorising every single transaction.

You’ll notice your spending naturally falls into a couple of key buckets:

- Fixed Expenses: These are the predictable bills that stay the same month after month. Think mortgage or rent, council tax, car insurance, loan payments, and your phone contract. They’re easy to list.

- Variable Expenses: This is where things get more interesting. These are the costs that change, like groceries, petrol, utilities (gas and electric can vary wildly), entertainment, and personal spending.

Don’t forget the budget-killers: those irregular expenses that pop up and cause chaos if you’re not ready. I’m talking about things like the annual car tax, Christmas and birthday gifts, or a yearly insurance premium. The trick is to create “sinking funds” for these. By setting aside a small amount each month, you’ll have the cash sitting there waiting when the bill finally arrives.

Step 3: Give Every Pound a Job Until You Reach Zero

Okay, this is the moment you bring it all together. You have your total income from Step 1 and your exhaustive list of expenses from Step 2. The whole point of zero-based budgeting is to make your income minus your outgoings equal exactly zero.

Start by allocating money to your non-negotiables first. Cover your housing, utilities, food, and transport. Next, direct money toward your big financial goals—this means hitting your debt repayment targets and making contributions to your savings or investments. Finally, whatever is left over can be assigned to your “wants,” like hobbies, entertainment, or subscriptions.

Income – (Fixed Expenses + Variable Expenses + Savings + Debt Repayments) = £0

If you’ve assigned money to every category and still have some left over, you’re not done yet! That surplus cash needs a job, too. Could you put an extra £50 toward your credit card debt? Or maybe move it straight into your emergency savings? On the flip side, if you find you’re short on money, it’s time to go back to your variable spending list and decide where you can trim the fat.

Step 4: Track Your Spending Through the Month

A budget is just a piece of paper (or a spreadsheet) until you actually follow it. This is the crucial part. Throughout the month, you have to diligently track every penny you spend and see how it lines up with your plan. It’s the only way to know if you’re staying on course.

This doesn’t have to be a painful manual process. There are fantastic budgeting apps out there like YNAB or Mint that connect to your bank accounts and categorise your spending for you. If you prefer a more hands-on approach, a simple spreadsheet works just as well, as long as you commit to updating it. To help you get started, we’ve put together a collection of free budget templates you can download and make your own.

Tracking your spending gives you real-time feedback. If you see you’re getting dangerously close to your “Groceries” limit halfway through the month, you know it’s time to rein it in.

Step 5: Review and Adjust for Next Month

Your budget isn’t a “set it and forget it” document. It’s a living, breathing plan that needs to adapt as your life changes. Carve out some time at the end of each month to sit down and review how things went.

Ask yourself some honest questions:

- Where did I overspend, and what was the reason?

- Which categories did I underspend in?

- Did any surprise expenses catch me off guard?

- Are my spending priorities still aligned with my long-term goals?

The answers will give you the insight you need to build next month’s budget. Maybe you consistently overspend on food and need to give that category a bit more breathing room, while cutting back on a subscription you don’t use. The aim is for constant improvement, tweaking your plan each month so it becomes an even more powerful tool on your journey to financial freedom.

Common Pitfalls and How to Make ZBB Work for You

Starting a zero-based budget is a fantastic move for your finances, but let’s be real—it’s not always a walk in the park. Building this new habit is more of a marathon than a sprint, and knowing where the hurdles are can help you sail right over them. It’s easy to start with a ton of enthusiasm, only to get tripped up by a few common challenges.

The trick to making ZBB stick for the long haul is to know what these pitfalls are and have a game plan ready. By understanding the common traps—like being too restrictive or getting buried in the details—you can turn this powerful method into a sustainable habit that truly works for you.

Forgetting About Irregular Expenses

One of the quickest ways to blow up a perfectly good budget is to forget about the expenses that only pop up once or twice a year. Think car tax, insurance premiums, or even the holiday gift-giving season. These costs can sneak up on you and throw your entire plan into chaos if you haven’t accounted for them.

The best way to handle these is with sinking funds. All this means is you break down a big, future expense into small, bite-sized monthly savings.

- Car Tax Example: If you know your car tax is £180 a year, you just set aside £15 every month. When the bill arrives, the cash is already sitting there, ready to go.

- Christmas Fund: Want to have £600 for gifts and festivities? That’s just £50 a month tucked away, starting in January.

This simple bit of planning transforms a potential budget emergency into just another line item, keeping things predictable and stress-free.

Being Too Rigid with Your Plan

When you first map out your zero-based budget, it’s tempting to make it airtight. The problem is, life isn’t airtight. An unexpected car repair, a last-minute dinner invitation, or a surprise vet bill can make it feel like you’ve failed. This is where a lot of people get frustrated and give up.

A successful budget needs a bit of flexibility to survive contact with reality. Your plan should be a guide, not a financial straitjacket.

The solution? Build a ‘Miscellaneous’ or ‘Buffer’ category right into your budget from the start. This is a small stash of cash—maybe £50 or £100—that doesn’t have a specific job. It’s there to absorb the little surprises life throws at you. If you get to the end of the month and haven’t touched it, great! You can roll it over or put it toward one of your bigger financial goals.

Suffering from Tracking Burnout

The idea of manually logging every single coffee, snack, and bus ticket is enough to make anyone’s head spin. Honestly, tracking burnout is one of the biggest reasons people abandon ZBB. If you’re trying to do it all with a notebook and pen, it can quickly feel like a draining chore, leading to missed transactions and an inaccurate budget.

This is where a little bit of tech can be your best friend. Modern budgeting apps do most of the heavy lifting by syncing with your bank accounts and automatically categorizing your spending. This frees you up to focus on the big picture, not the tiny details. For a deeper dive, check out our guide on how to track expenses without it taking over your life. Automating the grunt work is the key to making your zero-based budget a simple, sustainable habit.

Common Questions About Zero-Based Budgeting

Starting a zero-based budget for the first time usually brings up a handful of practical questions. Let’s get those sorted out so you can jump in with confidence.

Here are a few of the most common things people ask when they’re getting started.

How Do I Manage a Variable Income with ZBB?

This is a big one, but ZBB is actually one of the best methods for handling an income that goes up and down. The trick is to build your monthly budget based on your lowest realistic income—your baseline.

Then, you decide ahead of time exactly what you’ll do with any extra money you bring in. When a good month hits, you’re not scrambling; you already know that surplus is going straight toward paying off your credit card faster or beefing up your emergency fund.

How Long Does Creating a ZBB Take Each Month?

I’ll be honest, that first month is the toughest. You’ll probably spend a solid two or three hours digging through statements and tracking down all your spending to create your categories.

But it gets so much easier. Once you have that initial template, most people find they can plan out the next month’s budget in less than an hour. It just becomes a quick monthly check-in.

What Are the Best Tools for Zero-Based Budgeting?

You have great options here. Apps like YNAB (You Need A Budget) and EveryDollar are built from the ground up for this style of budgeting and make the process pretty slick.

If you’d rather not pay for an app, a simple spreadsheet works just as well. It’s more of a manual approach, but it gives you total control.