Table of Contents

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

If you're serious about cutting your expenses, you have to know exactly where your money is going. It's not about guesswork. The real work begins with a financial deep dive—an audit, really—to see the unfiltered truth of your spending habits. From there, you can spot the big-ticket items that are draining your account and start making targeted cuts that don't feel like a major sacrifice.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

The entire idea is to make deliberate choices that actually line up with what you want for your future, not just what you want in the moment.

Your Path to Financial Control Starts Here

Getting a grip on your finances isn't about restrictive budgeting. It's about shifting from being a passenger, constantly reacting to bills and financial worries, to being the driver of your own financial future. Learning how to trim the fat from your budget is a skill, and it’s the foundation for escaping financial anxiety and achieving your biggest goals.

Forget the vague advice you've heard before. We're going to get into real, actionable methods that put you in charge. This is about transforming your mindset from one of scarcity to one of strategic control, which is the only way to build lasting financial health. The aim is to free up your cash so it can work on what really matters to you, whether that's wiping out debt, building a safety net, or investing for long-term financial freedom.

The Mindset Shift for Lasting Change

Before we even touch a spreadsheet, the most important work happens in your head. You have to stop seeing this as a punishment. Cutting expenses is an act of empowerment, not restriction. Seriously. Every dollar you intentionally save is a dollar you're giving to your future self.

Think of it this way: You're not "giving up" your daily $5 latte. You're "investing" that $1,825 a year into your financial independence. That small perspective flip can be the difference between sticking with it and giving up after a week.

This whole process is about making sure your daily spending habits align with your biggest dreams. It ensures your money is a tool working for you, not against you. And this journey isn't just about the numbers; it's also about protecting your well-being. For more on that, check out our guides on health, lifestyle, and well-being on a budget, which can help you stay balanced while you work toward your goals.

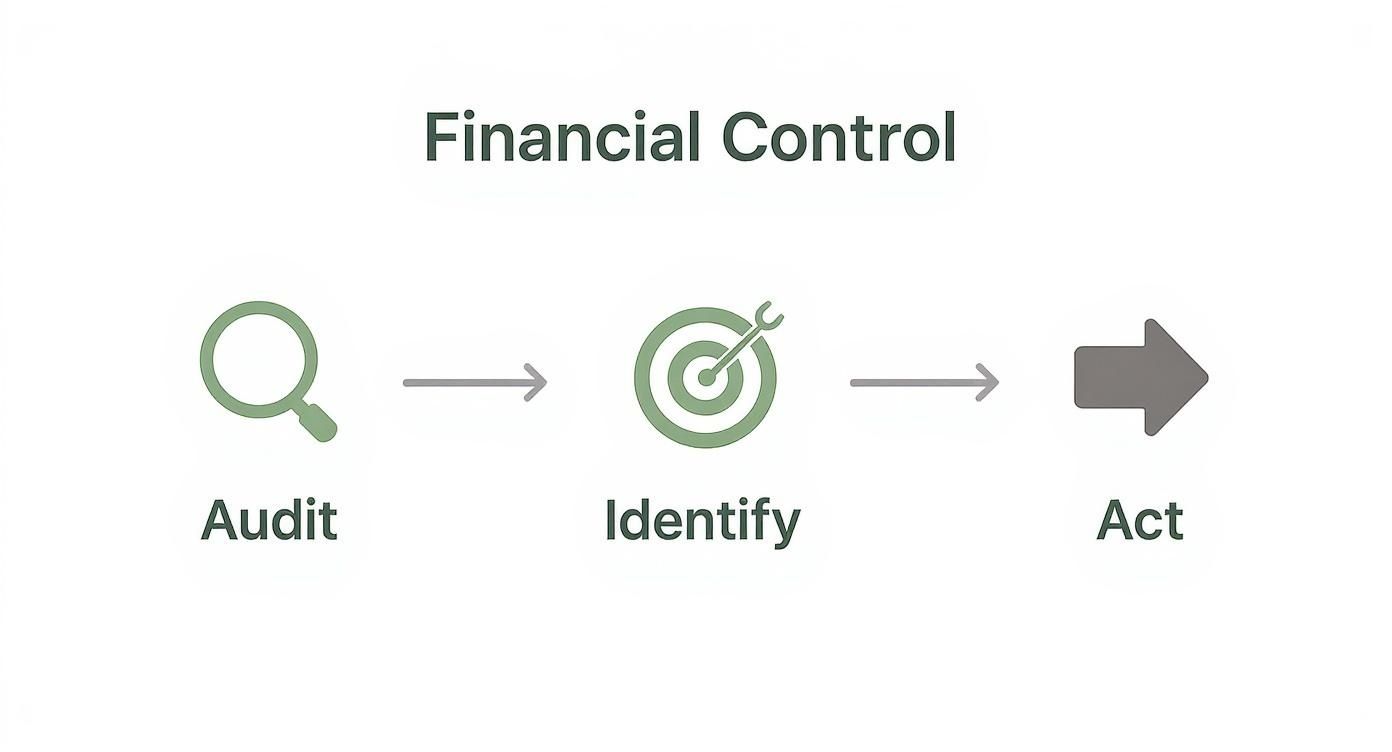

The infographic below breaks down the simple, three-part process for taking back control.

This visual roadmap gets straight to the point: you have to understand your habits (Audit), pinpoint the problem areas (Identify), and then take meaningful steps to fix them (Act).

Get to Grips With Your Spending: A No-Nonsense Financial Audit

Before you can plug the leaks, you have to find them. The first step in taking back control of your finances is to become a detective in your own life and conduct a thorough financial audit. This isn't about feeling guilty about past purchases; it’s about gathering intelligence to make smarter, more conscious decisions moving forward.

Thankfully, you can ditch the dusty shoebox full of receipts. Technology makes this process surprisingly straightforward. Budgeting apps like YNAB (You Need A Budget) or Mint can connect directly to your bank accounts, automatically tracking and sorting your spending for you. Many high street bank apps now have excellent built-in spending analysis tools that give you a clear, visual breakdown of your habits with just a few taps.

Sorting Your Spending to Reveal the Truth

The whole point of this exercise is to sort every transaction into a clear category. Doing this forces you to confront your actual financial habits, not just what you think you spend. Generally, every expense you have will fall into one of three buckets:

- Fixed Expenses: These are the big, predictable costs that stay roughly the same each month. We're talking about your mortgage or rent, council tax, and any loan repayments.

- Variable Expenses: These are the essentials that can fluctuate from month to month depending on your choices and usage. This covers things like groceries, utility bills, and transport costs.

- Discretionary Expenses: This is everything else—all the "wants" rather than the "needs." It includes streaming services, gym memberships, entertainment, hobbies, and personal care.

Categorising your spending this way is incredibly powerful. It immediately shows you where you have the most leverage. While you can't slash your mortgage in half tomorrow, you have 100% control over your discretionary spending right now.

A financial audit isn't about restriction. It's about discovering where your money is quietly leaving your wallet without your permission. Once you see the patterns, you reclaim the power to direct that money toward what truly matters.

Uncovering Those Sneaky Spending Leaks

Let me give you a real-world example. A couple I know, Sarah and Tom, felt like they were always broke despite earning decent salaries. They decided to link their accounts to a budgeting app and review the last three months of their bank statements together.

What they found was shocking. They were spending over £70 a month on forgotten subscriptions—an old gym membership, a streaming service they rarely watched, and a premium app Tom didn't even remember buying. This is a classic case of subscription creep, where tiny monthly charges quietly bleed your account dry.

But that wasn't all. They discovered another huge leak: mindless daily spending. Their routine of grabbing coffee on the way to work and other small daily purchases was costing them nearly £300 a month. Each purchase seemed insignificant on its own, but the cumulative effect was massive. By looking at the hard data, they weren't guessing anymore. They had a clear, actionable list of expenses they could cut immediately to accelerate their path to financial freedom.

A Simple Framework for Categorizing Your Expenses

Use this simple framework to sort your own spending. This will help you get organised and see exactly where your money is going, highlighting the areas with the biggest potential for savings.

| Expense Category | Type (Fixed, Variable, Discretionary) | Example | Potential for Reduction (High, Medium, Low) |

|---|---|---|---|

| Housing | Fixed | Mortgage/Rent | Low |

| Utilities | Variable | Electricity & Gas | Medium |

| Loan Repayments | Fixed | Car Loan/Personal Loan | Low |

| Transportation | Variable | Fuel, Public Transport | Medium |

| Groceries | Variable | Weekly Food Shop | Medium |

| Subscriptions | Discretionary | Streaming Services, Gym | High |

| Entertainment | Discretionary | Cinema, Concerts, Hobbies | High |

| Personal Spending | Discretionary | Shopping, Gifts, Coffee | High |

Laying it all out like this gives you a clear roadmap. You now know exactly which categories to target to make the biggest impact on your budget and get you closer to your financial goals.

Making Strategic Cuts to Major Expenses

Once you've taken a hard look at where your money is going, a pattern usually emerges. The bulk of your spending is likely tied up in just a handful of big-ticket categories. If you really want to move the needle on your savings, you have to think beyond skipping the occasional coffee.

The real game-changers are the strategic cuts you make to your largest expenses: housing, transport, and debt. This isn't about miserable penny-pinching. It's about making smart, targeted adjustments that can free up hundreds, if not thousands, of pounds every year. This is where your effort will have the biggest impact on your financial future.

Optimizing Your Housing Costs

For most of us, our single biggest expense is keeping a roof over our heads. It's easy to feel like this is a fixed cost you can't control, but that's not entirely true. Even small efficiencies here can compound into massive savings over time.

Homeowners have a particularly powerful tool at their disposal: tackling the mortgage. Playing around with a mortgage overpayment calculator can be a real eye-opener. You'll see exactly how chipping in a little extra each month can shave years off your loan and save you a fortune in interest.

Another big win is simply reviewing your mortgage rate. If your fixed-term deal is ending or you’ve been sitting on a standard variable rate (SVR) for years, you could be overpaying. Remortgaging to a more competitive rate is some upfront paperwork for a potentially huge long-term gain.

Your housing costs are more than just the mortgage. Utilities, maintenance, and insurance all add up. By systematically reviewing each one, you're not just cutting a bill; you're optimising the financial performance of your biggest asset.

The wider economic climate often forces our hand on these things anyway. For instance, recent forecasts point to a major slowdown in consumer spending, partly because the housing market is so tough right now. With existing home sales down 2.4% in early reporting periods from last year, families are having to dedicate more income to housing, making it critical to find savings. You can dig into these U.S. consumer spending trends on morganstanley.com.

Lowering Your Utility Bills

After the mortgage or rent, utility bills are the next obvious place to look for savings. It's so easy to just stick with the same energy provider for years, but that kind of loyalty rarely pays off.

- Switch Energy Tariffs: Hop on a comparison site to see if you can get a better deal. The process is surprisingly straightforward, and your new supplier does all the heavy lifting.

- Embrace Small Upgrades: Little changes really do add up. Swap old incandescent bulbs for energy-efficient LEDs, seal drafts around windows, and turn your thermostat down by just one degree. You'll barely notice the difference, but your bill will.

- Install Smart Tech: A smart thermostat learns your routine and heats your home efficiently, so you're not paying to warm an empty house. Smart plugs are also great for stopping "vampire drain" from electronics left on standby.

These moves don't just shrink your bills; they make your home run more efficiently, which is good for your wallet and the planet.

Re-evaluating Transportation Expenses

For many households, transportation is the number two expense, right after housing. This is especially true if you rely on a car. The real cost of running a vehicle is so much more than just the monthly payment.

When you add it all up, you’re paying for:

- Fuel: Constantly fluctuating and a major drain.

- Insurance: A significant fixed cost every year.

- Maintenance & Repairs: Often unpredictable and always expensive.

- Depreciation: The silent killer that drains your car's value every day.

The total can be staggering. Honestly compare that number to the cost of alternatives like public transport, cycling, or even a car-sharing service for occasional trips. You might be shocked at the potential savings. For some, even downsizing from two cars to one can completely transform their monthly budget.

Conquering High-Interest Debt

High-interest debt from credit cards and personal loans is like trying to run a race with weights tied to your ankles. It actively works against you, eating up your income with interest payments that barely touch the principal amount you owe.

Two of the most popular and effective battle plans are the debt avalanche and debt snowball methods.

| Debt Repayment Method | How It Works | Best For |

|---|---|---|

| Debt Avalanche | You hammer away at the debt with the highest interest rate first, making minimum payments on the rest. | People who want the most mathematically efficient route to save on interest. |

| Debt Snowball | You focus on paying off the smallest debt first, regardless of the interest rate, for a quick win. | People who need the motivation and momentum from seeing progress fast. |

Which one is better? It all comes down to your personality. Do you get a kick out of pure efficiency, or do you thrive on motivational boosts? The best strategy is the one you’ll actually stick with. Just pick one, commit, and start freeing yourself for good.

Taming Your Discretionary Spending and Subscriptions

Once you've got a handle on the big stuff like housing and debt, it's time to look at the spending that can really sneak up on you. This is where you can find some of the fastest wins for your budget. We're talking about everything from small daily purchases to that ever-growing list of monthly subscriptions quietly nibbling away at your bank balance.

Trimming these costs isn't about sucking all the fun out of your life. It’s about being deliberate. The goal is to make sure your money is going toward things that actually matter to you, not just disappearing on autopilot.

Putting an End to Subscription Creep

Ever heard of "subscription creep"? It's that subtle, almost invisible process where a few small monthly charges—for streaming, apps, and memberships—add up to one surprisingly large bill. You’d be amazed at how much money can be tied up in services you've completely forgotten about.

The first step is to perform a full subscription audit. Pull up your last three months of bank and credit card statements and highlight every single recurring payment. Then, get honest with yourself and ask a few tough questions for each one:

- Do I actually use this? If you haven't opened that app in months, it’s time to let it go.

- Is it genuinely worth the cost? Does the value it provides justify the price tag?

- Could I find a free alternative? Lots of paid services have great free versions that do the job just as well.

Once you’ve sorted your list into "keep" and "cancel," it's time to take action. Cancel the unnecessary ones right away—don't wait. For the ones you need, like your mobile phone or internet, see if you can get a better deal.

You'd be surprised what a quick phone call can achieve. Simply tell your provider you're reviewing your budget and ask if they have any loyalty discounts or newer, cheaper plans. The worst they can do is say no, but you might just save yourself some cash.

How to Master Your Impulse Spending

Beyond subscriptions, a lot of discretionary spending comes down to psychology. Retailers are masters of temptation, but you can fight back with a few simple mind tricks. One of my favorites is the 30-day rule.

It’s incredibly simple: when you see a non-essential item you want, don't buy it. Instead, write it down and wait 30 days. If you still want it just as badly after a month, then you can think about buying it. More often than not, the urge will have completely passed.

This creates a "cooling-off" period that helps you separate an emotional "want" from a genuine "need." It puts you back in the driver's seat of your spending decisions.

This kind of proactive money management is becoming more widespread, especially as living costs rise. In fact, recent data shows that 72% of young adults have started managing their finances more carefully. Of that group, 41% cut back on dining out, and 23% switched to more affordable grocery stores. You can dig into the full details about these financial habits of young adults on bankofamerica.com.

This shift shows that people are becoming much more intentional with their money. If you're looking for more ways to make your budget work for you, our guide on how to save money on groceries has a ton of practical tips. Adopting these habits isn't just about saving money today—it’s about building a foundation for a more secure financial future.

Building Your Sustainable Financial Future

Cutting your expenses is a powerful first step, but it’s not the end game. The real goal is to take that newly freed-up cash and build a rock-solid financial foundation. This is where you shift from constantly patching holes in your budget to constructing a fortress that genuinely protects you from money worries and helps you achieve financial freedom.

The absolute first priority on this journey? Building an emergency fund. Think of this as your financial shock absorber. It’s what turns a potential catastrophe—like a sudden job loss or a surprise car repair—into a manageable inconvenience, keeping you out of debt when life throws a curveball.

Why an Emergency Fund Is Your Top Priority

A proper emergency fund should hold enough cash to cover three to six months of essential living expenses. We’re talking about the non-negotiables: rent or mortgage, utilities, food, and transport. This money needs to be liquid and accessible, ideally in a separate high-yield savings account where it's out of sight but within reach.

I know, saving three to six months of expenses can sound intimidating. Don't let the final number paralyze you. The trick is to start small and build momentum. Your first goal could be just £500. Set up an automatic transfer for whatever you can afford on payday, even if it’s only £20. Consistency is what builds the habit and, eventually, the fund.

This financial safety net has never been more important. With the rising cost of living, many people are feeling the squeeze. In fact, 73% of Americans said they were saving less due to inflation. It's a worrying trend, with only 40-43% of households feeling good about their savings, a steep decline from 54% in 2020. You can read more about these emergency savings trends on bankrate.com.

From Saving to Investing for the Future

Once your emergency fund is in a healthy place, the real fun begins. The extra money you’re saving each month can now be put to work, growing your wealth and paving the way to true financial freedom.

You don't need a finance degree to start investing. For most people, simple and effective options are the best way to go:

- ETFs (Exchange-Traded Funds): Think of these as a pre-packaged bundle of investments. Instead of picking individual stocks, you buy a small piece of many companies at once (like the entire S&P 500), which automatically diversifies your risk.

- Index Funds: These work much like ETFs, aiming to simply match the performance of a market index. They are famous for their low fees and are a brilliant, hands-off way to build wealth over the long haul.

The secret weapon in your investing toolkit is compound interest. This is where your investment earnings start generating their own earnings. It creates a snowball effect that, over decades, can turn small, consistent investments into a massive nest egg.

Making the leap from saving to investing is a huge step in mastering your money. If you want to explore this further, our complete guide to money management skills is the perfect next read. Remember, the money you save today isn’t just for getting by—it’s the raw material for building the life you want tomorrow.

Got Questions About Cutting Expenses? We've Got Answers.

As you start looking for ways to trim your budget, a few questions always seem to pop up. Let's tackle some of the most common ones so you can move forward with a solid, confident plan.

How Much Can I Realistically Cut From My Budget?

This is the million-dollar question, isn't it? The honest answer is: it's completely personal. While popular guidelines like the 50/30/20 rule (50% for needs, 30% for wants, 20% for savings) are a decent starting point, they're not a one-size-fits-all solution.

Your perfect target depends on your income, how much debt you're carrying, and what you're trying to achieve. Instead of fixating on a random percentage, aim for a number that feels challenging but not impossible. The goal is to build a plan you can actually stick with long-term, not a crash diet for your wallet.

What Are the Best Apps to Help Me Track My Spending?

Using an app can feel like having a financial assistant in your pocket. It takes the guesswork out of tracking and shows you exactly where your money is going. Two of the best out there are:

- YNAB (You Need A Budget): This one is a fan favorite for a reason. Its philosophy is about being intentional and giving every single dollar a job. If you want to take a very hands-on, proactive approach, YNAB is fantastic.

- Mint: A great free option from Intuit, Mint connects to all your accounts automatically. It sorts your transactions, lets you see your net worth, and even keeps an eye on your credit score, all in one place.

The secret is finding one that clicks with you. Don't be afraid to try a couple and see which one you actually enjoy using.

I Feel Like I've Cut Everything Possible. What's Next?

First off, if you've already trimmed all the fat from your budget, that's a huge win. Seriously, give yourself credit for mastering a skill most people struggle with. Once you've made your spending as efficient as possible, the next logical step is to flip the equation: focus on increasing your income.

After you've optimized your spending, boosting your income is the most powerful lever you can pull. It dramatically speeds up your progress toward saving, investing, and hitting your biggest financial goals.

This doesn't have to mean getting a second job (though that's an option). You could build a compelling case for a raise at your current one. Or maybe you could develop a few high-demand skills that open the door to better-paying roles. Even a small side hustle built around something you enjoy can make a surprising difference.

At Collapsed Wallet, our entire mission is to give you clear, no-nonsense advice for managing your money. We want to help you build a more secure financial future, one smart decision at a time. To learn more, visit us at https://collapsedwallet.com.

3 thoughts on “How to Cut Expenses for Financial Freedom”