Table of Contents

- Building Your Financial Foundation as a Single Parent

- Creating Your Financial Safety Net and Tackling Debt

- Growing Your Income and Finding the Support You Deserve

- Investing for Your Future and Your Children’s Dreams

- Planning Ahead to Protect Your Family

- Your Step-By-Step Financial Action Plan

- Answering Your Top Financial Questions

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

Financial planning for single parents can feel like juggling on a unicycle. It’s not just about managing money on one income; it’s about creating a solid foundation that brings security and peace of mind for you and your kids. Getting a handle on your budget, building a safety net, and making smart choices about the future is how you move from feeling stressed to feeling empowered.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Building Your Financial Foundation as a Single Parent

Stepping into single parenthood means wearing a lot of new hats, and the “Chief Financial Officer” hat can feel especially heavy. If you’re feeling overwhelmed by it all, you are definitely not alone. A staggering 75% of single parents report feeling overwhelmed, and it’s no wonder many put off big money decisions.

In fact, research shows that four in 10 single parents don’t start planning for their child’s future until they are four to six years old, or even later. You can see more on this in the full research on lifehappens.org.

But here’s the thing: taking control of your money is the very first step toward building the stable, secure life you want for your family. It all starts with a simple but powerful mindset shift. See this not as a burden, but as an act of empowerment and a gift to your children’s future.

Mastering Your Budget and Cash Flow

A realistic budget is the bedrock of any solid financial plan. Forget the idea that budgeting is about restriction—it’s about clarity. A budget is simply a tool that tells your money where to go, making sure every pound has a job, whether that’s paying the electric bill or saving for a family holiday.

Think of it like planning a road trip. You wouldn’t just get in the car and start driving without a map and a destination in mind, right? A budget is your financial map, guiding you toward your goals, whether that’s getting out of debt, buying a home, or just having a less stressful month. It all starts with getting a crystal-clear picture of what’s coming in and what’s going out.

To help you get started, I’ve put together a quick checklist of the first few essential steps.

Your Financial Planning Quick-Start Checklist

| Action Step | Why It’s Crucial | First Task |

|---|---|---|

| Track Your Spending | You can’t manage what you don’t measure. This step uncovers where your money is really going. | Grab a notebook or use a budgeting app to log every single expense for one full month. |

| Categorize Expenses | This brings order to your spending, splitting it into fixed costs (rent), variable costs (groceries), and savings. | Group your tracked expenses into buckets like Housing, Utilities, Transport, and Childcare. |

| Set Financial Goals | Goals give your budget a purpose. They’re your “why,” turning what feels like a chore into a mission. | Write down one short-term goal (like building a £500 emergency fund) and one long-term goal. |

Once you’ve completed these steps, you’ll have a much better handle on your cash flow and be ready to build a budget that works for you. If you need some practical strategies for making it work, check out our guide on how to budget on a low income.

Choosing the Right Budgeting Method

There’s no single “best” way to budget. The right method is simply the one you can stick with. A popular and flexible starting point is the 50/30/20 rule, which you can easily adapt for a single-income household.

- 50% for Needs: This chunk covers your non-negotiable essentials. Think mortgage or rent, utilities, insurance, childcare, and transportation.

- 30% for Wants: This is for the “nice-to-haves”—discretionary spending like streaming services, hobbies, and family entertainment.

- 20% for Savings & Debt Repayment: This is the powerhouse portion. It’s dedicated to building your emergency fund, paying down debt, and investing for your future.

If dedicating 20% to savings feels impossible right now, don’t sweat it. Start smaller. Even saving 5% or 10% consistently will build powerful momentum. The secret is to make it automatic. Set up a direct transfer to move money from your current account to a separate savings account the day you get paid. This “pay yourself first” strategy ensures your future is always a priority, not an afterthought.

Creating Your Financial Safety Net and Tackling Debt

As the only one bringing in an income, you are the financial bedrock of your family. That’s a huge responsibility. The next critical step is to reinforce that bedrock with two things that are absolutely non-negotiable: a solid emergency fund and a smart plan to get out of debt. Think of them as your financial safety net, working together to protect your family from life’s curveballs.

Life happens. The car breaks down, a medical bill shows up out of the blue, or the boiler gives up in the middle of winter. These things can throw a tight budget into complete chaos. An emergency fund is your personal shock absorber, giving you the cash to handle these bumps without reaching for a high-interest credit card.

Building Your Emergency Fund Brick by Brick

I get it—the idea of saving three to six months of living expenses can feel completely overwhelming on one salary. But here’s the secret: you don’t have to get there overnight. The key is to just start.

Your first goal isn’t a massive pile of cash; it’s just getting some momentum. Aim for a starter fund of £500 or £1,000. Honestly, that amount is often enough to cover most of those annoying, unexpected expenses and will give you immediate breathing room.

The easiest way to make this happen is to automate it. Set up a standing order to transfer a set amount into a separate, high-yield savings account the day you get paid. This “pay yourself first” strategy makes saving a priority without you even having to think about it. For more practical tips, check out our detailed guide on how to build an emergency fund.

This financial cushion is about so much more than money. It’s about reducing stress. It creates a buffer between you and the panic of an unexpected bill, letting you make clear-headed decisions for your family.

Once you’ve hit that initial goal, keep contributing until you have 3 to 6 months of essential living expenses tucked away. This covers the absolute must-haves: rent or mortgage, utilities, food, childcare, and transport.

Developing a Smart Debt Reduction Strategy

Debt, especially the high-interest kind from credit cards and personal loans, can feel like a heavy anchor dragging you down. It eats into your monthly income and adds a constant layer of stress. Tackling it head-on is one of the most empowering things you can do for your financial future.

Two of the most popular and effective ways to pay down debt are the Debt Snowball and the Debt Avalanche. The best one for you really just depends on what makes you tick.

Choosing Your Debt Repayment Method

Let’s break down how each one works. Both strategies start the same way: you make the minimum payments on all your debts. The difference is where you put any extra money you can find.

Here’s a quick look at the two approaches:

| Method | How It Works | Best For |

|---|---|---|

| Debt Snowball | You throw every spare penny at your smallest debt first, no matter the interest rate. Once it’s gone, you take that entire payment amount and “roll it” onto the next-smallest debt. | People who thrive on quick wins. Seeing a debt completely disappear gives you a huge psychological boost and the motivation to keep going. |

| Debt Avalanche | You focus on paying off the debt with the highest interest rate first. Once that’s cleared, you move on to the one with the next-highest rate. | People who are driven by the numbers. This method will save you the most money in interest payments over the long run. |

No matter which path you choose, the end goal is the same: to systematically wipe out your debt and free up your money. Once a debt is gone, that cash can be redirected to other important goals, like topping up your emergency fund, saving for your kids’ future, or investing in your own retirement. You’re turning a source of worry into a challenge you can absolutely conquer.

Growing Your Income and Finding the Support You Deserve

A solid financial plan isn’t just about making cuts; it’s also about growing what you have. Once your budget is in place and you have a handle on debt, the next powerful move is to look for ways to increase your income. This two-pronged approach—boosting your earnings while tapping into the support systems you’re entitled to—can dramatically change your family’s financial future.

Making Your Main Job Work Harder for You

Your primary job is the engine of your household. Giving it a tune-up can be one of the most effective things you do for your finances, and that often starts with a conversation about your pay.

Asking for a raise can feel nerve-wracking, I get it. The key is to walk in prepared. Don’t just ask—build a case. Keep a running list of your accomplishments, note how you’ve contributed to the company’s goals, and do your homework on what others in your role and industry are earning. When you approach the conversation with facts and figures, it’s no longer an emotional request; it’s a business discussion.

If a raise isn’t a possibility right now, think about a flexible side hustle. There are so many options that can fit around the chaotic schedule of a single parent.

- Use your professional skills: Are you a whiz with words, design, or social media? Platforms like Upwork or Fiverr can connect you with projects you can tackle from your couch after the kids are asleep.

- Tap into the gig economy: Things like virtual assistance, online tutoring, or transcription work often let you set your own hours, working in the evenings or on weekends.

- Turn a hobby into cash: If you love creating, an Etsy shop could be a great way to turn that passion into a little extra income.

The idea isn’t to work yourself into the ground. It’s about finding a sustainable way to add another stream of income that can help you hit your savings goals or pay off debt that much faster.

Don’t Leave Money on the Table: Unlock Support Systems

One of the biggest financial mistakes I see single parents make is not claiming the support that’s available to them. Many are eligible for significant financial help but never apply, either because they don’t know it exists, the paperwork seems overwhelming, or they simply don’t think they’ll qualify.

Let’s be clear: using these resources is not a handout. It’s a smart, strategic financial move. These programs were created to provide a safety net and help you build a stable foundation for your family.

The financial reality for single parents can be tough. The numbers don’t lie: 27% of US single-parent families live below the federal poverty line. That’s more than four times higher than the 6% for married-couple families, according to eye-opening research from the Annie E. Casey Foundation. This is exactly why it’s so critical to use every single resource at your disposal.

Key Programs and Credits to Look Into

Trying to figure out government assistance can feel like a maze, but it helps to know what you’re looking for. These programs are specifically designed to take some of the pressure off, especially for families with one provider.

Here are the most important areas to investigate:

- Tax Credits: These are pure gold because they reduce your tax bill dollar-for-dollar. The Child Tax Credit and the Child and Dependent Care Credit are two of the biggest game-changers for parents. Tax rules can and do change, so make it a habit to check the latest guidelines every year to make sure you’re claiming every penny you deserve.

- Childcare Subsidies: The cost of childcare can feel like a second mortgage. Government programs can help cover a chunk of this expense, making it possible for you to work or go back to school. Eligibility is usually tied to your income and family size.

- Housing and Utility Help: You might be able to get assistance with rent or find programs that lower your heating and electricity bills. This can free up a surprising amount of cash in your monthly budget for other essentials.

A great place to start is your state or federal government’s official website, which usually has a central hub for benefits and tools to check your eligibility. Applying for this support isn’t just another thing on your to-do list—it’s an active step toward giving yourself some much-needed breathing room.

Investing for Your Future and Your Children’s Dreams

When you’re juggling everything day-to-day, planning for “someday” can feel like a luxury you just don’t have time for. But investing is what turns those distant dreams—a comfortable retirement, college for the kids—from giant worries into actual, achievable goals. It might sound intimidating, but the idea behind it is simple and incredibly powerful.

Think of it like planting a small money tree. You start with a little seed (your first investment), and with time and patience, it grows into something real. The secret sauce is compound interest, which is just a fancy way of saying your earnings start making their own earnings. That’s how real wealth is built.

The Power of Starting Small and Simple

You absolutely do not need a pile of cash to get started. The most critical part isn’t how much money you begin with, but how soon you begin. Thanks to the magic of compounding, even small, regular contributions can blossom into a serious nest egg over the years.

And forget the stressful image of a stock-picker glued to a screen. The good news? You don’t have to do any of that. Simpler, hands-off options are often the best bet for building wealth without the headache.

- Exchange-Traded Funds (ETFs): Picture buying a single share that’s like a basket holding tiny pieces of hundreds of companies. That’s an ETF. It instantly diversifies your money, so all your eggs aren’t in one basket.

- Index Funds: These are built to simply match a major market index, like the S&P 500. It’s a low-cost, set-it-and-forget-it approach that lets you ride the market’s long-term growth.

These tools take the guesswork out of the equation. If you want to get a better handle on the basics, our guide on how to start investing for beginners breaks it all down in plain English.

Using Tax-Advantaged Accounts to Supercharge Growth

One of the smartest moves you can make is to invest using special accounts that give you a serious tax break. These are designed specifically for big goals like retirement and education, and they help your money grow much faster.

Using tax-advantaged accounts is like giving your investments a turbo boost. By shielding your money from taxes, you get to keep more of your returns working for you.

Here are the key accounts every single parent should have on their radar:

| Account Type | Primary Goal | Key Benefit |

|---|---|---|

| 401(k) or Workplace Pension | Retirement | Employer matching is free money. Don’t leave it on the table! |

| Individual Retirement Account (IRA) | Retirement | Get tax deductions now (Traditional) or tax-free withdrawals later (Roth). |

| 529 Plan | Education | Your money grows and comes out tax-free for qualified education costs. |

Balancing Your Retirement and Your Child’s Education

It’s completely natural to want to pour every spare dollar into your child’s college fund. But here’s a piece of advice you’ll hear from every financial expert: secure your own retirement first. It sounds selfish, but it’s not.

Your kids can find loans, scholarships, and grants for college. There are no loans for retirement.

Think of the safety instructions on an airplane—you have to put your own oxygen mask on before you can help anyone else. By making sure you’re financially stable in your later years, you’re giving your children the incredible gift of not having to support you.

A great place to start is by contributing enough to your 401(k) to get the full company match. That’s a guaranteed 100% return on your money. Once that’s handled, you can start putting money into a 529 plan for your child. Even small, steady contributions over 18 years can grow into a massive help when those tuition bills finally show up.

Planning Ahead to Protect Your Family

As a single parent, you wear a lot of hats, but the most important one is being your child’s protector. This means we have to think about some of the tough “what if” scenarios. This isn’t just about spreadsheets and numbers; it’s about making sure your kids are safe and secure, no matter what happens. It’s one of the most powerful ways to show your love and give yourself real peace of mind.

Let’s dive into two of the most important things you can do: getting the right insurance to protect your income and setting up a basic estate plan to protect your children.

Insurance: Your Financial Shield

Think of insurance as a financial shield. It’s there to step in and provide for your family if you’re suddenly unable to, making sure a personal tragedy doesn’t turn into a financial one, too. For a single parent, two types are absolutely essential.

Life Insurance is a must-have, plain and simple. If you were to pass away, a life insurance policy gives your family a tax-free lump sum of money. This can replace your income for years to come, pay off big debts like a mortgage, and even cover your kids’ college tuition. It’s the ultimate back-up plan to ensure they are looked after financially.

Disability Insurance is just as crucial. Here’s a startling fact: you’re far more likely to become disabled during your working years than you are to die. This insurance acts as a replacement for your paycheck if you can’t work because of an illness or injury, allowing you to keep paying the bills and running your household.

Choosing the Right Life Insurance Policy

The world of life insurance can feel a bit overwhelming, but honestly, for most single parents, it really just comes down to two main options.

| Policy Type | How It Works | Best For |

|---|---|---|

| Term Life Insurance | You get coverage for a set amount of time, like 20 or 30 years. It’s straightforward, affordable, and purely focused on protection. | The vast majority of single parents. It’s designed to get you the most coverage for the lowest cost, protecting your kids until they’re grown and financially independent. |

| Whole Life Insurance | This is a permanent policy that covers you for your entire life. It combines the insurance with a savings component, which makes it a lot more expensive. | People with very specific, complex financial needs or those who have dependents who will need lifelong care. For most, term life is the smarter, more practical choice. |

For most of us, term life insurance is the clear winner. It’s a simple and incredibly cost-effective way to get the protection your family needs without breaking the bank.

Think of it this way: a good policy ensures that even if you’re not there, your financial plans for your children’s future can continue without a hitch. It’s the ultimate safety net.

Estate Planning: The Most Important Promise You’ll Ever Make

“Estate planning” can sound intimidating and expensive, but for a single parent, it boils down to one absolutely critical document: a will.

A will is a legal document that spells out your wishes, but its most important job is to name a legal guardian for your minor children. This is huge.

If you don’t have a will, a judge who doesn’t know you or your family will make this decision. That’s a scary thought. Naming a guardian is probably the single most important thing you can do to ensure your kids are raised by someone you love and trust if you’re not around.

Your will also guides how your assets are handled, making sure everything you’ve worked so hard for goes directly to your kids. While you’re setting this up, take a few minutes to update the beneficiaries on all your accounts—like your retirement plan, bank accounts, and insurance policies—to match what’s in your will. This simple bit of planning is your final, lasting promise to protect your family.

Your Step-By-Step Financial Action Plan

Alright, let’s pull all of this together. We’ve covered a lot of ground, from budgeting basics to long-term retirement goals. Think of those as the individual tools in your financial toolkit. Now it’s time to lay them out in a clear, step-by-step plan that you can actually start using today.

This is where the theory stops and the action begins. We’ll turn that mountain of “should-dos” into a series of manageable steps. The idea here is to build momentum. Small, consistent wins are what create huge, life-changing results down the road.

Phase 1: The Immediate Priorities

These are the absolute must-dos. The non-negotiables. Getting these things handled first creates the solid ground you need to build everything else on. It’s like pouring the foundation for a house—you can’t skip it, and it has to be strong.

- Build a Real-World Budget: Don’t just guess. Spend a month tracking every penny coming in and going out. This gives you a brutally honest snapshot of your finances, which is the only way to create a budget that actually works for you and your family.

- Create a Starter Emergency Fund: The first goal is small and achievable: save £500 to £1,000. This isn’t about covering six months of unemployment; it’s about having cash on hand so a flat tire or a sick kid doesn’t send your finances into a tailspin. Set up an automatic transfer to a separate savings account—even a small one—and let it build.

- Check Your Insurance: As the sole provider, having the right life and disability insurance is your ultimate safety net. Make sure your coverage is enough to protect your children if something were to happen to you.

- Write Your Will: This is, without a doubt, the most important task for any single parent. A will is the only legal document that lets you name a guardian for your children. It ensures they are cared for by the person you choose and trust.

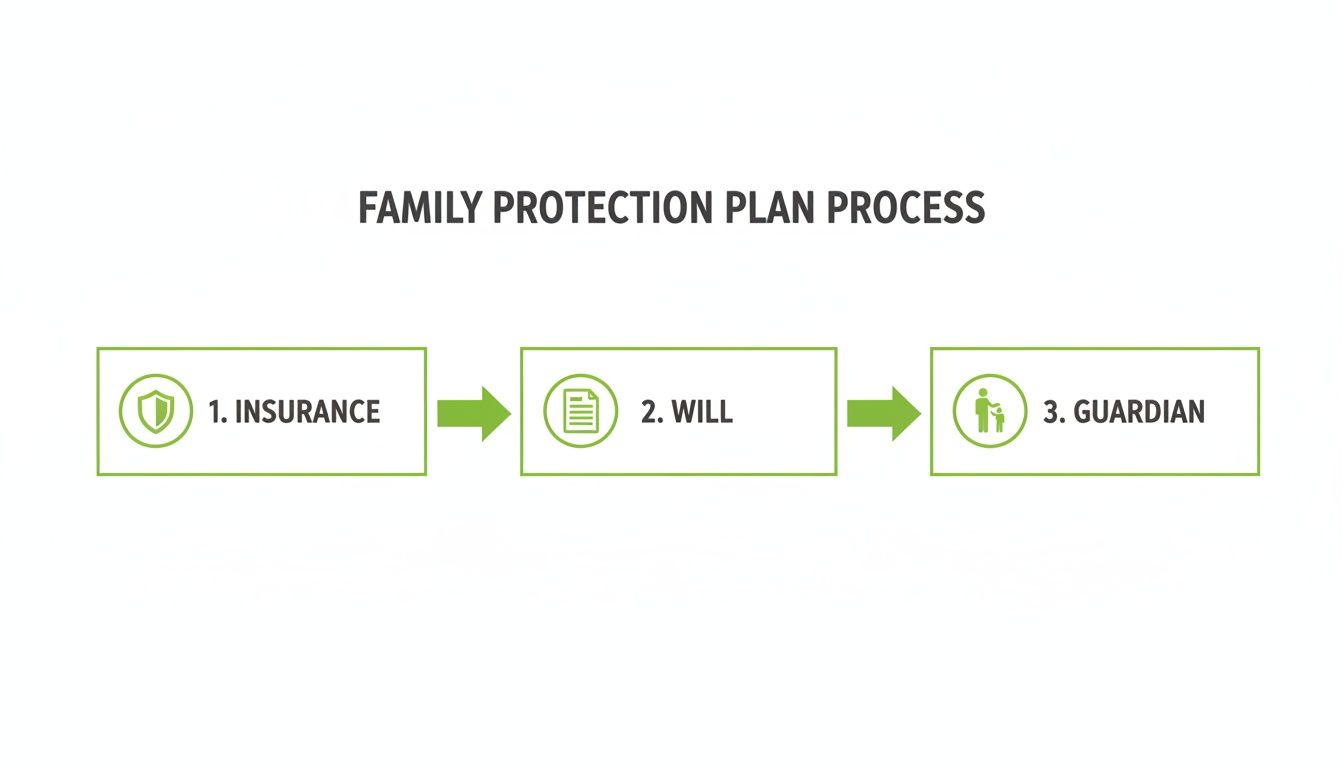

This flowchart breaks down the three core pieces of your family’s protection plan, which should be at the very top of your to-do list.

As you can see, these three elements—insurance, a will, and a named guardian—work together to form a complete circle of protection for your kids’ future.

Phase 2: Building Financial Strength

Once the foundation is solid, you can start building upwards. This next phase is all about getting rid of the things that are holding you back financially and starting to create some real forward momentum. This is where you’ll begin to feel a genuine sense of control.

Tackling high-interest debt is one of the most powerful moves you can make. Every pound you no longer pay in interest is a pound you can redirect toward your family’s future.

These medium-term goals are designed to free up your cash flow and get you moving faster:

- Attack High-Interest Debt: Pick a strategy that works for you, like the Debt Snowball or Debt Avalanche, and go after your credit cards and personal loans with a vengeance.

- Fully Fund Your Emergency Savings: Now it’s time to build on that starter fund. Keep saving until you have 3 to 6 months worth of essential living expenses tucked away.

- Find Ways to Boost Your Income: Could you ask for a raise at work? Is there a flexible side hustle you could start? Even a small increase in income can make a massive difference.

- Claim Everything You’re Entitled To: Double-check that you’re receiving all the tax credits, childcare subsidies, and government benefits you qualify for. Leaving this money on the table is a common and costly mistake.

By working through these phases in order, the whole process of financial planning feels less overwhelming and much more achievable. Every single step you complete is a victory, building the stable, prosperous future your family deserves.

Answering Your Top Financial Questions

As you start putting all these pieces together, a few big questions tend to pop up again and again. Let’s tackle two of the most common ones that single parents face.

Should I Save for My Retirement or My Kid’s College First?

This is a tough one, but the answer is surprisingly simple: your retirement has to come first. It can feel counterintuitive, but it’s the most responsible choice you can make for your family’s long-term health.

Think about it this way: your child has options for funding their education—scholarships, grants, and even student loans. But when it comes to retirement? There are no loans or scholarships for that. Your financial security in your later years depends entirely on the planning you do now.

The best gift you can give your child is ensuring you won’t be a financial burden on them later in life. A great starting point is to contribute enough to your workplace pension to get the full employer match. That’s free money, and you should never leave it on the table. After that, you can start putting money into a dedicated education account, like a 529 plan.

What’s the Smartest Way to Handle Child Support?

Child support can sometimes feel unreliable, which makes it tricky to budget around. The safest and most powerful strategy is to build a budget that works without it. Don’t count on it for your essential, day-to-day expenses.

Instead, when the payments do come in, treat them as a financial accelerant. You can use that extra cash to make some serious progress on your goals.

- Crush High-Interest Debt: Throw it at your credit card balance or personal loans.

- Supercharge Your Emergency Fund: Use it to hit that 3-6 month savings target faster.

- Invest in the Future: Add a little extra to your retirement fund or your child’s college savings.

This way, if a payment is late or missed, your core household budget remains stable and secure. But when the money arrives, you can put it to work making a real difference.

Here at Collapsed Wallet, our mission is to give you the clear, practical guidance you need to build a life of financial security. For more guides on budgeting, saving, and investing, explore everything we have to offer at https://collapsedwallet.com.