Table of Contents

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

If you’re serious about getting better with money, the first thing you need is a brutally honest look in the mirror. You have to know exactly where you stand right now—what you own, what you owe, and where every single dollar is going. This isn’t about judging past mistakes; it’s about getting a clear starting point so you can build a real plan that actually works. Here you will find everything you need to know to help you manage money better!

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Laying Your Financial Foundation

You can’t build a solid house on a shaky foundation, and the same goes for your finances. Before you can even think about building wealth or getting out of a financial rut, you need to understand your starting point. It’s all about gaining clarity.

This process really boils down to two key numbers: your net worth and your monthly cash flow. Get these two figures down, and you’ll have a powerful snapshot of your current financial health.

First, Figure Out Your Net Worth

Your net worth is the ultimate scoreboard for your finances. It’s a simple but powerful calculation: what you own (your assets) minus what you owe (your liabilities).

- Assets: This is everything of value you have. Tally up the cash in your bank accounts, the current value of any investments (ETFs, retirement accounts), what your home and car are worth today, and any other significant valuables.

- Liabilities: This is the other side of the coin—all your debts. List out your mortgage balance, car loans, student debt, credit card balances, and any personal loans.

Subtract your total liabilities from your total assets, and that’s your net worth. The number might be positive, negative, or zero. It doesn’t matter. What matters is that you know it, because this is the number you’re going to work on improving.

Your net worth is your financial North Star. It gives you a baseline to measure your progress and shows you how every single decision—every dollar saved, every investment made, every debt paid down—moves you closer to your goals.

Next, Map Your Cash Flow

If net worth is a snapshot, cash flow is the movie of your money. It’s the story of what comes in and—more importantly—what goes out every month. The best way to understand this is to track your spending for at least 30 days.

This used to be a pain, but technology has made it incredibly easy. Most banking apps automatically categorize your transactions for you. If you want more power, dedicated budgeting apps can sync with all your accounts to give you a complete picture of your spending habits.

The goal here is to see what you’re spending on essentials (like housing) versus the wants (like that daily coffee or multiple streaming subscriptions). You’ll almost certainly uncover some “spending leaks”—those small, forgotten costs that are draining more from your account than you realize.

To get started, don’t overcomplicate it. Use this simple table to get a quick overview of where your money is going right now.

Your Quick-Start Financial Snapshot

Use this simple template to quickly assess your current financial health by mapping out your income, core expenses, and debt obligations.

| Financial Category | Your Monthly Amount ($) | Actionable Goal |

|---|---|---|

| Total Monthly Income (After Tax) | e.g., Increase by 5% this year | |

| Housing (Rent/Mortgage) | e.g., Keep under 30% of income | |

| Utilities (Electric, Water, Gas) | e.g., Reduce by $20/month | |

| Transportation (Car, Gas, Public) | e.g., Find cheaper insurance | |

| Groceries & Food | e.g., Lower restaurant spend by $100 | |

| Total Monthly Debt Payments | e.g., Pay off one credit card |

Jotting down these core numbers will give you a much clearer picture and help you set realistic, actionable goals for the coming months.

Finally, Check Your Debt-to-Income Ratio

One last crucial piece of the puzzle is your debt-to-income (DTI) ratio. This percentage tells you how much of your gross monthly income is already spoken for by debt payments. If that number is high, it leaves you with very little room to save, invest, or handle an emergency.

Across the board, many households are stretched thinner than they think. In the United States, for example, total household debt reached about $18.59 trillion in Q3 2025. This staggering figure highlights why a written budget isn’t just a nice-to-have anymore—it’s essential. It’s the only way to see if your fixed costs are suffocating your ability to get ahead. You can dig into more data on this from the New York Fed’s quarterly report.

Crafting a Budget That Actually Works

Let’s be honest, the word “budget” can make you want to run for the hills. It often brings up images of restrictive spreadsheets and saying “no” to everything fun. But a good budget does the exact opposite—it’s your personal roadmap to financial freedom.

It’s not about deprivation. It’s about giving your money a purpose.

The secret to finally getting a handle on your money is to find a budgeting method that actually fits your life. If it feels like a chore, you’ll drop it within a month.

Find Your Budgeting Style

There’s no one-size-fits-all answer here. The best budget for you is the one you’ll actually stick with. Think of these popular methods as starting points, not rigid rules.

- The 50/30/20 Rule: This is a fantastic, low-stress starting point. The idea is to divide your after-tax income into three buckets: 50% for your Needs (rent/mortgage, utilities), 30% for Wants (hobbies, entertainment), and 20% for Savings and Debt Repayment. Simple and effective.

- Zero-Based Budgeting: If you’re someone who likes precision and control, this is for you. Every single dollar gets a job. Your income minus all your expenses—including savings—has to equal zero at the end of the month. It takes more effort but gives you an incredible sense of where every penny is going.

- Pay Yourself First: This is less of a full-blown budget and more of a powerful habit to build. The moment your paycheck hits, an automatic transfer sends a set amount to your savings or investment accounts. You do this before paying any bills or spending a dime. The rest is yours to manage, knowing your goals are already covered.

The most successful people often mix and match. You might use the 50/30/20 rule as a guideline but still automate your savings by paying yourself first.

Uncover Your Hidden Spending Leaks

With a framework in mind, it’s time to play detective and figure out where your money is really going. This is usually the most eye-opening part of the process.

Those little purchases—the daily coffee, that forgotten subscription, the late-night online buy—are the culprits. They seem harmless, but they can easily add up to hundreds of dollars a month.

A budget isn’t about restricting your freedom; it’s about creating it. By telling your money where to go, you gain the power to build the life you want instead of wondering where your money went.

Pull up your bank and credit card statements from the last 30 days and start categorizing everything. Don’t overcomplicate it.

Start with these simple categories:

- Housing: Rent or mortgage

- Utilities: Electricity, water, internet, phone

- Transportation: Car payment, gas, insurance, transit passes

- Financial Goals: Savings, debt payments, investments

- Debt: Credit cards, student loans

- Personal: Subscriptions, gym, shopping, entertainment

As you sort through your spending, patterns will jump out at you. You might be shocked at your entertainment bill or realize you have three streaming services but only watch one. These are your spending leaks, and they’re the easiest places to find extra money for your goals without feeling deprived.

Set Realistic Limits (Without Sucking the Joy Out of Life)

Here’s where most budgets fail: they’re completely unrealistic. If you create a budget that slashes your spending in half overnight or forbids you from ever enjoying your hobbies, you’re setting yourself up to fail.

Your budget needs to bend with your life, not break it.

Start with small, sustainable adjustments. Instead of banning restaurants, maybe you trim your dining-out fund by 20%. Instead of axing all your subscriptions, just cancel the one you use the least. These small wins build momentum and prove to you that you can do this.

To make things even easier, let technology do the heavy lifting. There are some fantastic tools out there, and you can check out some of the best free budgeting apps to find one that automates expense tracking for you. An app gives you real-time feedback, helping you stick to your plan without having to manually log every single purchase.

Put Your Money on Autopilot

Let’s be honest: relying on willpower to manage your money every single day is exhausting. It’s why so many of us start strong with a budget but fall off track a few weeks later. The single most powerful shift you can make is to take your moment-to-moment decisions out of the equation.

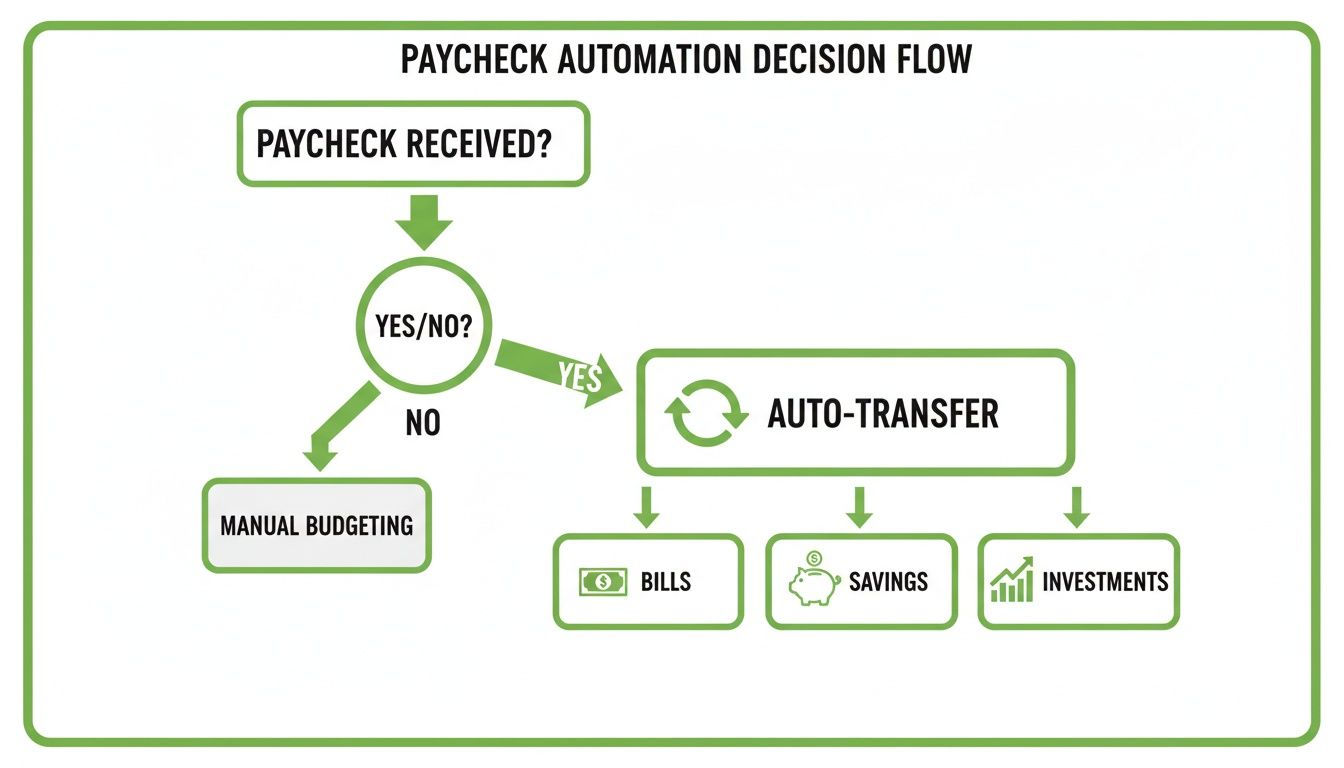

The real secret to consistent progress isn’t more discipline—it’s building a smart, automated system. By setting things up once, you can make sure your money goes exactly where it needs to, right when you get paid, without you lifting a finger. It’s like putting your financial goals on autopilot.

Pay Yourself First, Automatically

You’ve probably heard the phrase “pay yourself first.” It means funding your future before you pay your bills or buy anything else. Automation is what makes this concept a reality.

The idea is to have a series of transfers kick off the second your paycheck lands in your account. You can set this up in just a few minutes through your bank’s online portal or app. Just schedule recurring transfers for your payday.

Here’s where that money should go:

- Your High-Yield Savings Account: This is for your emergency fund and any short-term goals you’re working toward. Automating this transfer ensures you’re constantly building that crucial cash cushion.

- Your Investment Accounts: Whether it’s a retirement account or a brokerage account for ETFs, small, consistent contributions are the key to building long-term wealth. Let compounding do the heavy lifting for you.

- A Dedicated Debt-Payoff Fund: If you’re aggressively paying down high-interest debt, automatically moving extra money into a separate account ensures you make consistent headway.

When you do this, saving is no longer an afterthought—something you do with whatever is “left over.” It becomes a fixed, non-negotiable expense, and you simply learn to live on the rest.

Automate Your Bills and Protect Your Credit

Late fees are a 100% avoidable waste of money. Even worse, a single missed payment can ding your credit score and stick around for years. The easiest win in personal finance is automating your bills.

Virtually every company, from your landlord and utility provider to your credit card issuer, offers an auto-pay option. Set it up. This one small action removes the risk of forgetting a due date, saves you from pointless fees, and protects the credit score you’ll need for big life goals like buying a home.

Automating your savings and bills makes your best financial intentions the default. It removes the daily temptation to overspend and the mental stress of juggling due dates, freeing up your energy for the bigger picture.

Let Technology Do the Work for You

We’re lucky to live in an age where fantastic financial technology can do most of the hard work. Modern apps can securely link to your bank accounts and give you a complete, real-time picture of your money without you ever having to touch a spreadsheet.

Think of these tools as a 24/7 personal finance assistant. Many popular budgeting apps can turn your financial plan from a list of numbers into a clear, visual dashboard.

This kind of visual feedback makes it so much easier to see where your money is going and track your progress. Many of the best savings apps offer similar tools that automatically categorize your spending, track your net worth, and even find new ways for you to save.

This instant insight helps you make smarter choices on the fly and keeps you connected to your goals without the grind of manual tracking.

Your Strategic Plan to Eliminate Debt

High-interest debt can feel like you’re trying to swim with an anchor tied to your ankle. It just grinds down your financial progress, making it feel impossible to get ahead. But you can absolutely break free. It’s not about some get-rich-quick scheme; it’s about creating a smart, strategic plan to systematically chip away at what you owe and finally take back control.

The real key is shifting your mindset. You have to move from just making those depressing minimum payments to actively and aggressively attacking your balances. It’s a change in focus, and it needs a solid strategy to keep you fired up.

Choosing Your Debt Repayment Method

When it comes to the actual “how,” there are two fantastic, time-tested methods: the debt snowball and the debt avalanche. Honestly, neither one is universally “better.” The best one for you comes down to your personality and what gets you excited to keep going. The most effective plan is always the one you’ll actually stick with.

The Debt Snowball Method

This strategy is all about psychology and momentum. Think of it as a series of small, satisfying wins. You list all your debts from the smallest balance to the largest, completely ignoring the interest rates for a moment. You’ll keep making the minimum payment on every single debt, but you throw every extra dollar you can find at that smallest one first.

Once it’s gone—poof!—you get this huge psychological boost. You did it. Then, you take all the money you were paying on that now-dead debt (the minimum plus all the extra cash) and “roll it” onto the next-smallest debt. This creates a “snowball” of money that just gets bigger and bigger as you knock out each balance, building an incredible momentum that makes it easier to stay in the fight.

The Debt Avalanche Method

If you’re someone who loves spreadsheets and is driven by pure numbers, the debt avalanche is probably your jam. For this one, you list your debts from the highest interest rate to the lowest, ignoring the balance size. Again, you make minimum payments on everything, but you funnel all your extra money toward the debt with the highest interest rate.

This approach is the most efficient, saving you the most money in interest over the long haul because you’re wiping out the most expensive debt first. While the initial wins might feel a bit slower than the snowball, the long-term financial payoff is bigger. It’s the mathematically perfect way to clear your debt.

Deciding between the snowball and avalanche isn’t just a math problem—it’s a behavior problem. Choose the strategy that lights a fire under you. A small, consistent win that keeps you in the game is far more valuable than a “perfect” plan you abandon after a month.

Debt Snowball vs Debt Avalanche: A Comparison

Still not sure which path to take? This table breaks down the key differences between these two popular debt repayment strategies to help you find the best fit for your financial style.

| Feature | Debt Snowball Method | Debt Avalanche Method |

|---|---|---|

| Primary Focus | Psychological wins & motivation | Mathematical efficiency & saving money |

| Debt Order | Smallest balance to largest balance | Highest interest rate to lowest |

| Best For | People who need quick wins to stay motivated | People driven by numbers and long-term savings |

| Pros | Builds momentum fast, highly motivating | Saves the most money on interest over time |

| Cons | May cost more in interest over time | Initial progress can feel slow, less motivating |

Ultimately, both roads lead to the same destination: being debt-free. Your job is to pick the one that you’ll enjoy driving on the most.

Exploring Other Debt Management Tools

Beyond these core strategies, a few other tools in the financial toolbox can help you manage and even speed up your journey out of debt. Just remember, these aren’t magic wands and you need to think carefully before using them.

- Debt Consolidation: This is where you take out a new, single loan (often a personal loan) to pay off a bunch of smaller debts. The main goal is to simplify everything into one monthly bill, hopefully at a lower interest rate than your credit cards. This works wonders, but only if you have the discipline to stop using the credit cards you just paid off.

- Balance Transfers: You’ve probably seen the offers: credit cards with 0% APR for an introductory period. A balance transfer lets you move your high-interest credit card debt over to one of these new cards. This gives you a window of time, often 12-18 months, to pay down the principal without getting hammered by interest charges. Just be aware of the transfer fee (usually 3-5% of the balance) and make absolutely sure you can pay it off before that promo period ends and the rate skyrockets.

This decision tree shows how you can put your paycheck on autopilot to funnel money toward your most important financial goals, including getting out of debt.

When you set up these kinds of automatic transfers, you guarantee that a piece of every single paycheck goes right where it needs to—toward your debt, savings, and investments—without you having to lift a finger.

For a much deeper dive into these methods, check out our comprehensive guide on how to pay off debt fast. It’s packed with more strategies and detailed steps to help you build the perfect plan. Tackling debt is a journey, not a sprint, so remember to celebrate the small victories along the way. It’s what keeps you going until you finally achieve that financial freedom.

Building Savings and Investing for Your Future

Managing your money well isn’t just about cutting costs and paying down debt. That’s playing defense. The real shift happens when you start playing offense—making your money actively work for you. This transition rests on two powerful pillars: building a solid savings cushion and starting to invest for your long-term goals.

These two pieces work hand-in-hand to create genuine financial security. Savings act as your shield against today’s emergencies, while investing is your engine for building the wealth you’ll need for tomorrow’s dreams, like retirement or true financial independence.

The Non-Negotiable Emergency Fund

Before you even think about investing a single dollar, you need a financial safety net. This is your emergency fund, and it’s arguably the most critical savings goal you’ll ever have. It’s a dedicated pot of cash, tucked away in a high-yield savings account, for one purpose only: to cover unexpected, essential expenses.

Think of it as the buffer between you and life’s inevitable curveballs—a sudden job loss, a major car repair, or an unexpected medical bill. Without this fund, these events can easily force you into high-interest debt, completely derailing your financial progress.

The rule of thumb is to save 3-6 months’ worth of essential living expenses. To figure out your number, just add up your non-negotiable monthly bills:

- Housing (rent or mortgage)

- Utilities (electricity, water, internet)

- Transportation (car payment, fuel, insurance)

- Essential spending (groceries, healthcare)

- Minimum debt payments

Multiply that monthly total by three, and you’ve got your initial target. The best way to build it is to automate a weekly or bi-weekly transfer to your savings account. It doesn’t matter if it’s a small amount; just get it started and watch it grow. This single step is a game-changer for reducing financial anxiety.

An emergency fund isn’t an investment; it’s insurance. It’s not there to make you rich—it’s there to stop you from becoming poor when something goes wrong.

Demystifying Investing for Beginners

Once your emergency fund is in a healthy place, it’s time to put your money to work. Investing can sound intimidating, but the core concept is actually quite simple: you’re buying assets that have the potential to grow in value over time, helping your money outpace inflation.

Good money management is about more than just personal habits; it’s about building a fortress against wider economic trends. With global debt hitting a record $338 trillion in the first half of 2025, according to the Institute of International Finance, personal financial resilience is more critical than ever. This macro-level risk underscores why having an emergency fund and investing for the future isn’t just smart—it’s essential. You can see how these trends affect households by reading the full Global Debt Monitor report.

For most people just getting started, the best approach is to keep things simple, low-cost, and diversified.

Harnessing the Power of Compounding and ETFs

The real magic behind long-term wealth creation is compound interest. This is the process where your investment earnings start generating their own earnings. Over decades, this creates a powerful snowball effect that can turn small, consistent contributions into a substantial nest egg.

A fantastic way to get started and tap into this power is through Exchange-Traded Funds (ETFs). The easiest way to think of an ETF is as a basket that holds hundreds or even thousands of different stocks or bonds all in one.

So, why are ETFs so great for beginners?

- Instant Diversification: When you buy a single share of a broad market ETF (like one that tracks the S&P 500), you’re instantly spreading your money across many different companies. This dramatically reduces your risk.

- Low Cost: ETFs almost always have much lower fees than traditional mutual funds, which means more of your money stays invested and working for you.

- Easy to Access: You can buy and sell ETFs through any online brokerage account with just a few clicks, often with no commission fees.

You absolutely do not need a lot of money to start. Many brokerages now offer fractional shares, meaning you can invest with as little as a few dollars. The most important thing isn’t how much you start with, but that you start now and stay consistent.

Questions We Hear All the Time

Jumping into managing your money can feel like learning a new language. You’re bound to have questions, and that’s a good thing! It means you’re engaged and ready to make a change.

Let’s clear up a few of the most common hurdles people face right at the beginning.

How Often Should I Actually Look at My Budget?

It’s tempting to create a budget, feel good about it, and then promptly forget it exists. But a budget isn’t a “set it and forget it” kind of tool. To really work, it needs your attention.

For most of us, a monthly check-in is the sweet spot. It’s frequent enough to catch small issues before they become big problems, but not so often that it feels like a full-time job. Once a month, sit down, compare what you planned to spend with what you actually spent, and see what needs tweaking.

That said, you’ll want to revisit your budget immediately if you hit a major life change. Things like:

- A new job, a pay raise, or a sudden loss of income.

- Big life events, like getting married, buying a house, or welcoming a new baby.

- A major shift in your goals, like deciding you’re ready to aggressively pay down debt.

I’m Completely Overwhelmed. Where Do I Even Start?

When you’re staring down a pile of bills and don’t know where your money is going, it’s easy to just freeze up. If you’re feeling that financial paralysis, I want you to do just one thing: track every dollar you spend for the next seven days.

That’s it. No changing your habits. No judging yourself for any purchases. Just write it down. Use a note on your phone, a pocket-sized notebook, whatever works.

This one small step is incredibly powerful for two reasons:

- It breaks the inertia. You’re taking a single, concrete action instead of worrying about a huge, complex plan.

- It gives you instant data. You’ll immediately see patterns and little “spending leaks” you had no idea existed.

Feeling overwhelmed isn’t a sign of failure; it’s a sign you need more information. Tracking your spending is the fastest way to trade anxiety for clarity.

Once you have that week of data, you’ll have a real foundation to build on. The fog starts to lift, and creating a full budget suddenly feels much more manageable.

What Makes an Expense Tracking App Actually Good?

The right app can be a game-changer, automating the tedious parts of money management. But with hundreds out there, it’s hard to know what to look for. Not all apps are created equal, especially when you’re just starting out.

Here are the non-negotiable features a good, user-friendly app should have:

- Automatic Bank Syncing: This is the big one. The app must securely link to your bank and credit card accounts to pull in your transactions automatically. Manual entry is a habit-killer.

- Customizable Spending Categories: Every app comes with defaults, but your life isn’t default. You need the ability to create categories that actually match your spending habits and priorities.

- Simple Visuals: A picture is worth a thousand numbers. Look for an app that uses clean charts and graphs to show you where your money is going. It makes spotting trends a breeze.

- Goal Tracking: Being able to set a goal—like saving $5,000 for an emergency fund—and watch your progress is a huge motivator.

- Rock-Solid Security: Make sure the app uses bank-level encryption. You’re trusting it with your most sensitive data, so there’s no room for compromise here.

Ultimately, the best app is the one you’ll actually use. Find one that feels intuitive and simple. If it’s a pain to navigate, you’ll drop it within a week.

Here at Collapsed Wallet, our goal is simple: to give you the straightforward, practical advice you need to build a better financial future. We cut through the jargon to offer actionable steps that help you take back control.

Ready to dive deeper? Explore more of our guides and resources at https://collapsedwallet.com.

2 thoughts on “How to Manage Money Better a Practical Guide to Financial Freedom”