Table of Contents

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

It’s the classic financial Catch-22: you want to pay down your debt, but you also know you need to be saving. So, which do you do first? The answer might surprise you—you don’t have to choose. The smartest way forward is to build a small safety net before you start throwing every spare penny at your debts. This is your ultimate guide to help you save money and pay off debt!

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Let’s walk through how to take control by tackling both goals at once, starting with the most important first step.

Your Starting Point for Financial Control

Starting a journey to become debt-free and build savings can feel like staring up at a huge mountain. The pressure from bills pulls you one way, while the dream of a secure future pulls you another. The secret isn’t to start by cutting back on everything. It’s to prepare. Before you go on the offensive against your debt, you need to build a financial firewall.

That firewall is a starter emergency fund. We’re not talking about a huge pile of cash here. Just a small, accessible reserve—somewhere around £500 to £1,000—set aside for genuine, unexpected emergencies. It’s the buffer that stops a flat tyre or a broken boiler from derailing your entire plan.

Why an Emergency Fund Comes First

Think about it. Without that cash cushion, what happens when an unexpected expense pops up? You’re forced to reach for a credit card or take out a small loan, putting you right back where you started. It’s a frustrating cycle, and it kills your motivation. A recent survey showed that nearly 40% of adults couldn’t cover a £400 emergency without going into debt. That one stat shows just how close to the edge many of us are living.

Building a small emergency fund is the most critical first step. It stops the cycle of borrowing for minor crises and gives you the stability needed to focus on a long-term debt repayment plan without constant setbacks.

To build this fund, you first need to know exactly where your money is going. Gaining that clarity is key. If you’re not sure where to begin, our guide on how to track your expenses breaks it down into simple, manageable techniques.

Once that starter fund is safely tucked away, you can pivot and start attacking your debt with real confidence. This two-pronged approach means you’re no longer just putting out financial fires—you’re proactively building a stronger future.

Build a Budget That Actually Works for You

Let’s get one thing straight: a budget isn’t a financial straitjacket. It’s your roadmap to freedom. It’s the tool that finally lets you see exactly where your money is going so you can start telling it where to go instead—like toward becoming debt-free and building a secure future.

You can forget about complicated spreadsheets for now. We’re going to start with a simple but incredibly powerful framework that just plain works: the 50/30/20 rule.

Popularized by Senator Elizabeth Warren, this method has been a game-changer for millions because it’s so easy to follow. You simply divide your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It’s not just a nice theory, either. One study found that 72% of households using this rule built an emergency fund of over $10,000 within just two years—a huge leap compared to only 39% of those who weren’t using it.

Breaking Down the 50/30/20 Rule

First things first, you need to know your take-home pay. This is the actual amount that lands in your bank account each month after taxes and deductions are taken out. Got that number? Great. Here’s how to split it up:

- 50% for Needs: This is for all your absolute essentials. Think rent or mortgage, utilities, groceries, and getting to work. These are the bills you have to pay every month to keep the lights on.

- 30% for Wants: This is the fun stuff! It covers everything that makes life more enjoyable but isn’t strictly necessary. We’re talking about dining out, your Netflix subscription, hobbies, and that weekend trip you’ve been dreaming of.

- 20% for Financial Goals: This is where the magic happens. This entire slice of your income is dedicated to your two biggest priorities: paying down debt and building up your savings.

That final 20% is your engine for progress. By consistently dedicating this chunk of your income to your goals, you create real, steady momentum without feeling like you’ve had to give up everything you enjoy.

Sample 50/30/20 Budget Breakdown

To make this crystal clear, let’s look at how the 50/30/20 rule works with a real-world income. This table shows a breakdown for someone taking home $4,000 per month after taxes.

| Category | Percentage | Example Monthly Amount (Based on $4,000) | What It Covers |

|---|---|---|---|

| Needs | 50% | $2,000 | Rent/Mortgage, Utilities, Groceries, Transportation, Insurance |

| Wants | 30% | $1,200 | Dining Out, Hobbies, Subscriptions, Entertainment, Shopping |

| Financial Goals | 20% | $800 | Extra Debt Payments, Emergency Fund, Retirement Savings |

As you can see, that $800 in the “Financial Goals” category is a powerful amount. It can be split between your starter emergency fund and making extra payments on your high-interest debt, accelerating your journey to financial freedom.

Making the Budget Work for You

The best part about the 50/30/20 rule is that it’s a guideline, not a law. What if your ‘Needs’ are creeping above 50% because you live in a high-cost-of-living area? That’s okay. You simply adjust by trimming your ‘Wants’ category to make up the difference. The one non-negotiable is protecting that 20% for your financial goals.

The key to a successful budget is not restriction, but intentionality. The 50/30/20 rule provides a clear framework to make conscious decisions about your spending, ensuring your money aligns with your long-term goals of financial stability and freedom from debt.

Let’s be honest, manually tracking every single penny is a pain. Thankfully, technology can do the heavy lifting. Many of the best free budgeting apps link directly to your bank accounts, automatically categorizing your spending and showing you exactly how you’re tracking against your 50/30/20 targets. Apps like YNAB (You Need A Budget) or Mint give you a real-time snapshot of your finances, making it almost effortless to stay on track.

Imagine this: you look at your app and realize that reducing discretionary spending frees up an extra $50 a month. That might not sound like much, but when you throw that $50 into your ‘Financial Goals’ bucket, it can shave months off your debt repayment plan and save you a bundle in interest. That’s the empowering clarity a good, simple budget provides.

Choosing Your Debt Repayment Strategy

Alright, you’ve got your budget dialed in and have freed up some cash to throw at your goals. Now for the big question: what’s the smartest way to attack that debt?

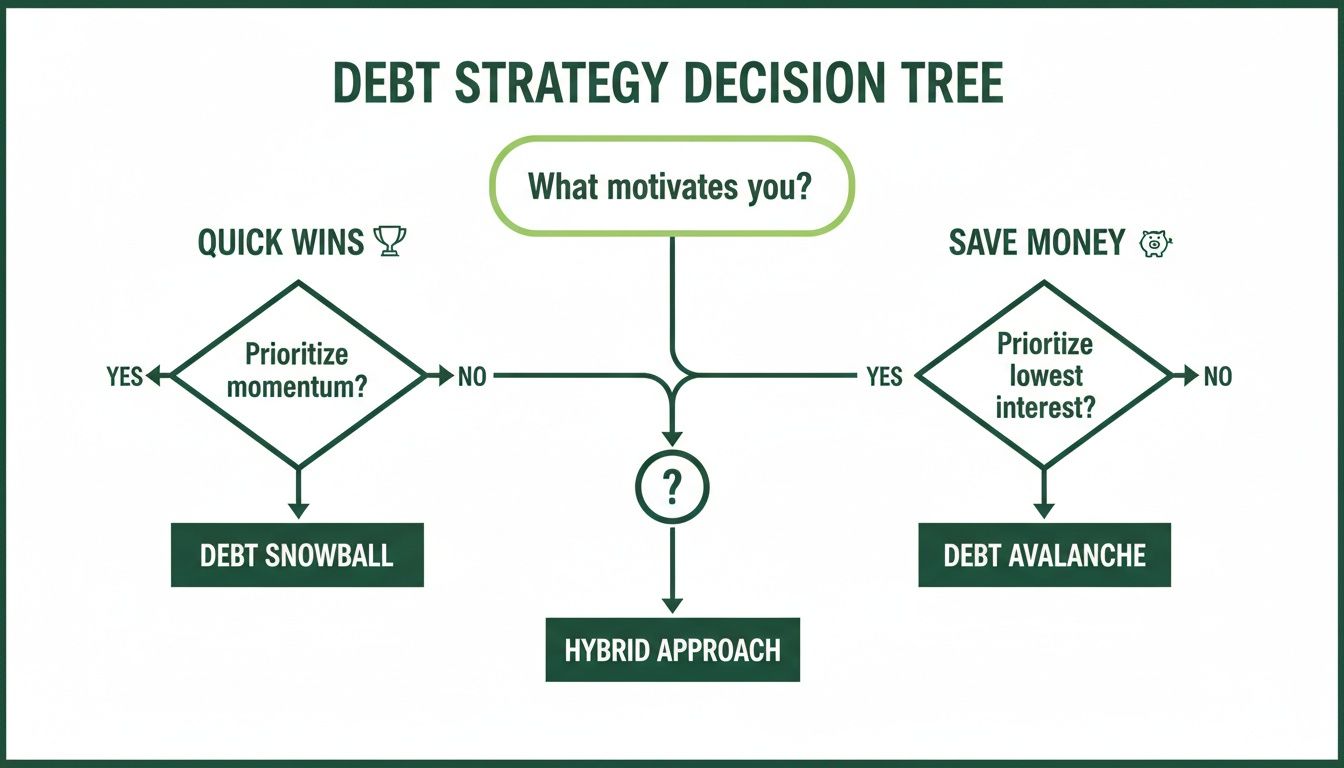

When it comes to paying off what you owe, there’s no single right answer. It really boils down to what makes you tick. The two most popular and effective methods are the Debt Snowball and the Debt Avalanche. Your choice comes down to a simple question: Are you motivated by quick, satisfying wins, or by knowing you’re making the most efficient financial move possible?

Let’s dig into how each one works so you can figure out which strategy will light a fire under you and keep you going.

The Debt Snowball: Small Wins for Big Momentum

The Debt Snowball method is pure psychology. It’s designed for people who thrive on seeing progress, and it uses that feeling to build unstoppable momentum.

Here’s the game plan: You list out all your debts from the smallest balance to the largest, completely ignoring the interest rates. You’ll keep making the minimum payments on everything, but every spare pound you have goes toward wiping out that smallest debt first.

Once it’s gone—poof—you get a huge jolt of accomplishment. You did it! Then, you take the entire amount you were paying on that cleared debt (the minimum plus all the extra cash) and roll it onto the next-smallest debt. This is where the “snowball” effect kicks in. As you knock out each debt, the payment you’re making on the next one gets bigger and bigger, clearing it even faster.

The real magic of the Debt Snowball isn’t about saving the most money—it’s about staying in the fight. Those early victories give you the psychological boost you need to stick with it for the long haul, which is often the biggest hurdle to clear.

The Debt Avalanche: The Mathematically Superior Path

If the Snowball is about emotion, the Debt Avalanche is all about the cold, hard numbers. This strategy is for anyone whose main goal is to pay the least amount of interest possible over time.

With the Avalanche, you line up your debts by interest rate, from highest to lowest. The actual balance doesn’t matter here. You’ll still make the minimum payments on all your debts to stay in good standing. But every extra penny is aimed squarely at the debt with the highest interest rate—usually a credit card with a punishing APR.

This approach is brutally effective. By targeting your most expensive debt first, you stop it from racking up huge amounts of interest, which saves you a ton of money in the long run.

The Debt Avalanche delivers undeniable mathematical wins. With interest rates on the rise, credit card APRs have been averaging over 20%. Studies show that people using the Avalanche method can save 25-30% more on interest than those using the Snowball. In places like Australia, where household debt is high, official data reveals much faster payoff rates for those who prioritize their high-interest debts. You can find more about global debt trends on Wikipedia.

Debt Snowball vs. Debt Avalanche: A Head-to-Head Comparison

So, which path should you take? It’s a personal call. This table breaks down the key differences to help you decide which one fits your personality and financial situation best.

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Primary Focus | Psychological Wins: Builds motivation through quick, frequent victories. | Mathematical Efficiency: Saves the most money on interest over time. |

| Debt Order | Smallest balance to largest balance. | Highest interest rate to lowest interest rate. |

| Best For | Individuals who need to see progress to stay motivated and avoid burnout. | Individuals who are disciplined, numbers-driven, and focused on the bottom line. |

| Key Benefit | High success rate due to sustained motivation and positive reinforcement. | Minimizes total interest paid, leading to lower overall cost and a faster payoff. |

| Potential Drawback | May cost more in interest over time if high-interest debts are large. | Can feel slow at the start if the highest-interest debt has a large balance. |

At the end of the day, the best strategy is the one you’ll actually stick with. If the idea of completely eliminating a small medical bill in a few months gets you excited, the Snowball is probably for you. If the thought of saving hundreds or even thousands in interest is what gets you out of bed in the morning, then the Avalanche is the clear winner.

There’s no wrong choice here. The only thing that matters is picking the one that keeps you moving forward on your journey of learning how to save money and pay off debt.

4. Find Ways to Speed Things Up

You’ve laid the groundwork with a budget and picked a debt payoff strategy. That’s a huge step. But now it’s time to really kick things into high gear. Think of it as moving from a steady jog to an all-out sprint toward your financial goals.

To get there faster, you need to attack the problem from both sides. It’s not just about managing the money you have; it’s about increasing what comes in while simultaneously cutting down the interest that’s eating away at your progress. Let’s look at how to do both.

Give Your Income a Boost

The quickest way to have more cash for savings and debt is to earn more of it. It sounds almost too simple, but you’d be surprised how many people don’t explore the options right in front of them. This doesn’t mean you need a dramatic career change or a soul-crushing second job.

Here are a few practical ideas:

- Ask for a Raise: If you’re a solid employee and haven’t had a pay review in a while, it might be time to ask. Do your homework first. Research what your role pays on the open market, pull together a list of your biggest achievements, and book a meeting with your boss to make your case.

- Monetize a Skill You Already Have: What are you good at? Maybe you’re a whiz with spreadsheets, a great writer, or have an eye for design. Platforms like Upwork or Fiverr are full of people looking for freelance help. It’s a flexible way to earn on your own schedule.

- Turn a Hobby into a Side Hustle: Do you love crafting, woodworking, or photography? You could sell your goods on a site like Etsy or offer your services to people in your local community. When you enjoy the work, it feels a lot less like work.

Even an extra £200 a month can make a massive difference when you throw it directly at your biggest financial goal.

Get Smart With Debt Consolidation

While you’re working on bringing more money in, you also need to stop so much of it from going out in the form of interest. High-interest debt, especially from credit cards, feels like you’re trying to walk up an escalator that’s going down. It’s exhausting and demoralizing.

This is where consolidation tools can be a game-changer, but you have to use them carefully. The two most popular options are balance transfer cards and personal loans.

- Balance Transfer Cards: These are brilliant. They typically offer a 0% introductory APR for a set period, often between 12 and 21 months. You move your high-interest balances over, and suddenly, every single penny you pay goes toward clearing the actual debt, not just feeding the interest monster.

- Debt Consolidation Loans: If you have several different debts (cards, store credit, etc.), a personal loan can wrap them all into one. You’ll have a single monthly payment, usually at a fixed interest rate that’s much lower than what you were paying on your credit cards. It simplifies everything and can save you a bundle.

A word of warning: The goal here is to reduce your interest costs, not to free up your old credit cards for a new spending spree. Without discipline, you can easily end up in a worse position than when you started.

Always check the fine print before you sign up for anything. Watch out for balance transfer fees (they’re usually 3-5% of the amount you move) and make a note of when that 0% APR period ends. The best approach is to have a solid plan to clear the balance before the much higher standard interest rate kicks in.

Choosing the right overall debt strategy is the foundation. This decision tree can help you figure out if the Debt Snowball or Debt Avalanche is a better fit for your personality.

As you can see, it really boils down to what drives you. Are you motivated by quick, satisfying wins, or does saving the most money possible get you fired up? There’s no wrong answer—only the one that works for you.

Put Your Plan on Autopilot

Let’s be honest, the biggest hurdle to getting ahead with money isn’t a lack of knowledge. It’s consistency. The single best way to stay consistent? Take willpower out of the picture.

This is where automation becomes your secret weapon. When you build a financial system that runs on its own, you eliminate the daily mental tug-of-war over spending versus saving. You’re essentially creating a “set it and forget it” machine designed to make progress for you, even on days when you don’t feel like it.

Pay Yourself First—Always

You’ve probably heard the phrase “pay yourself first.” It’s a classic for a reason. Before you even think about paying bills or buying groceries, a slice of your income should go directly toward your savings and debt goals. Automation makes this a reality.

The moment your paycheck hits your checking account, you should have transfers lined up and ready to go. This isn’t just a nice idea; it’s how you guarantee you’re always moving forward.

Here’s what that looks like in practice:

- To Savings: An automatic transfer whisks your budgeted savings amount from your checking account to your high-yield savings account.

- To Debt: Another automatic payment sends your minimum payment—plus any extra you’ve committed—straight to your target debt.

By setting this up, you treat your financial goals like any other essential bill. They become non-negotiable.

How to Set Up Your Automated System

Putting this into motion is easier than you think. You can usually get it done in under an hour right from your bank’s website or mobile app. Just log in and find the section for recurring or automatic transfers.

Here’s my advice: schedule the transfer to your savings account for the day right after you get paid. That way, the money is moved before you even see it, squashing the temptation to spend it.

Next, set up all your debt payments to go out automatically. Not only does this keep you on track with your repayment plan, but it also saves you from the headache and cost of accidental late fees.

Automation is what turns good intentions into action. It builds positive financial habits directly into your system, ensuring you make progress whether you’re feeling motivated or not.

Keep an Eye on Your Progress

While automation handles the day-to-day work, “forgetting it” only applies to the manual effort, not your overall awareness. Watching your progress is the fuel that keeps you going for the long haul.

This is where a little tech can make a big difference. Seeing your debt balance drop and your savings climb is incredibly motivating. To see what’s out there, take a look at our guide to the best savings apps that can help you track your goals in a simple, visual way.

The psychological boost from seeing tangible results is powerful. It’s why strategies like the debt snowball work so well. Research from Northwestern University actually found that people who paid off their smallest debts first had a 15-20% higher success rate of becoming debt-free within two years. Why? Because those small, quick wins provided the motivation to keep going.

Ultimately, combining automated systems with mindful tracking creates a feedback loop that all but guarantees you’ll reach your financial goals.

From Debt-Free to Financially Free: What’s Next?

Making that final debt payment feels incredible, doesn’t it? It’s a moment of pure relief, the culmination of all your hard work and discipline. But after the initial celebration, it’s natural to wonder, “What now?”

The answer is powerful: you pivot. You shift your energy from erasing the past to building the future you want.

That significant chunk of cash you were sending to creditors every month? It just got a new job—working for you.

Shore Up Your Defenses

Before you dive into the exciting world of investing, let’s make sure your financial foundation is rock-solid. Remember that starter emergency fund you built? It’s time to turn it into a fortress.

Your goal now is to have three to six months of essential living expenses tucked away. This isn’t just a savings account; it’s your financial shock absorber. It protects you from life’s curveballs, like a sudden job loss or a medical emergency, so you can make future money moves from a place of confidence, not desperation.

Start Building Real Wealth

With a fully funded emergency fund in place, you can officially start your investing journey. I know investing can sound intimidating, but you don’t need to be a Wall Street guru to get started. The real secret is to just begin and keep it simple.

For most people, a fantastic starting point is low-cost exchange-traded funds (ETFs). Think of an ETF as a single investment that holds a diverse mix of stocks from hundreds or even thousands of companies. This built-in diversification is key—it keeps you from putting all your eggs in one basket.

The magic that makes this work so well over time is compound interest. This is where your investment earnings start making their own earnings. It creates a snowball effect that can grow your money exponentially over the long haul.

Shifting from debt repayment to investing is the final, crucial step. It’s where you take the discipline that got you out of debt and use it to build a secure, and even abundant, financial future.

By simply redirecting your old debt payments into smart, simple investments, you’re putting that same powerful focus toward long-term growth. This is the moment your financial journey truly begins to accelerate.

Got Questions? We’ve Got Answers

When you’re trying to tackle debt while saving for the future, a lot of questions pop up. It’s totally normal. Let’s walk through some of the most common ones people ask when they’re getting started.

Should I Save Money or Pay Off Debt First?

For almost everyone, the answer isn’t one or the other—it’s a mix of both. Your very first move should be to build a small starter emergency fund of about £500 to £1,000. Think of this as your financial firewall. It’s what stops a surprise car repair or an unexpected bill from immediately pushing you back into credit card debt.

Once you have that small safety net, you can pivot and get aggressive with your high-interest debt. You’ll throw most of your extra cash at your debts using the Snowball or Avalanche method, but you should still try to trickle a little bit into savings each month. The goal is to build your emergency fund while you simultaneously crush your debt.

How Long Will It Really Take to Become Debt-Free?

Honestly, this is different for everyone. How fast you can clear your debt comes down to three things: how much you owe, what your income is, and how much you can afford to pay above the minimums each month.

The best way to get a clear picture is to plug your numbers into a good online debt repayment calculator. You might be surprised at the results. For instance, finding an extra £150 per month to put towards a £10,000 credit card with a 20% interest rate could literally shave years off your repayment time and save you a fortune in interest.

The most common mistake is not creating a small emergency fund first. Without a cash cushion, a single unexpected event can force you to rely on credit cards again, adding to your debt and crushing your motivation.

What’s the Single Biggest Mistake People Make?

Hands down, it’s skipping the starter emergency fund. I get it—it feels completely backward to put money in a savings account when you have a mountain of debt glaring at you. But without that small cash reserve, you’re one flat tire away from a setback.

When an emergency happens without that buffer, the credit card is the only option. You not only add to your debt, but it’s a huge psychological blow. That small fund gives you the stability you need to stick with the plan for the long haul.

Is the Debt Snowball or Avalanche Method Better?

There’s no magic answer here. The “best” method is the one that you’ll actually stick with, and that really depends on what makes you tick.

- The Avalanche Method: This is the best choice from a pure math perspective. You target the debt with the highest interest rate first, which will always save you the most money over time.

- The Snowball Method: This method is all about psychology. You pay off your smallest debts first, regardless of the interest rate. Those quick wins create momentum and can be incredibly motivating, which helps a lot of people stay in the game.

So, if you’re a numbers person who loves efficiency, go with the Avalanche. If you need to see progress to stay fired up, the Snowball is your friend.

Here at Collapsed Wallet, we’re all about giving you clear, practical advice to help you get a handle on your money. For more real-world tips on budgeting, saving, and building a stronger financial future, check out the other guides on our site. You can find your path to financial freedom at https://collapsedwallet.com.