Table of Contents

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

When every pound is stretched to its limit, trying to save money can feel completely overwhelming. But getting a handle on your finances is more about building smart habits than making impossible sacrifices. It all starts with three fundamental moves: figuring out where your money is actually going, creating a simple plan for it, and then putting your savings on autopilot. Nailing these first few steps is what sets you up for real financial stability and gives you back that much-needed peace of mind.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Your Starting Point for Saving Money

The idea of saving when your budget is already tight can feel like a non-starter. But the secret isn't about making massive, painful cuts all at once. It’s about building a solid foundation, one that can support your financial goals for the long haul. Your journey really begins with these three core actions: understanding your spending, creating a roadmap, and making saving a reflex.

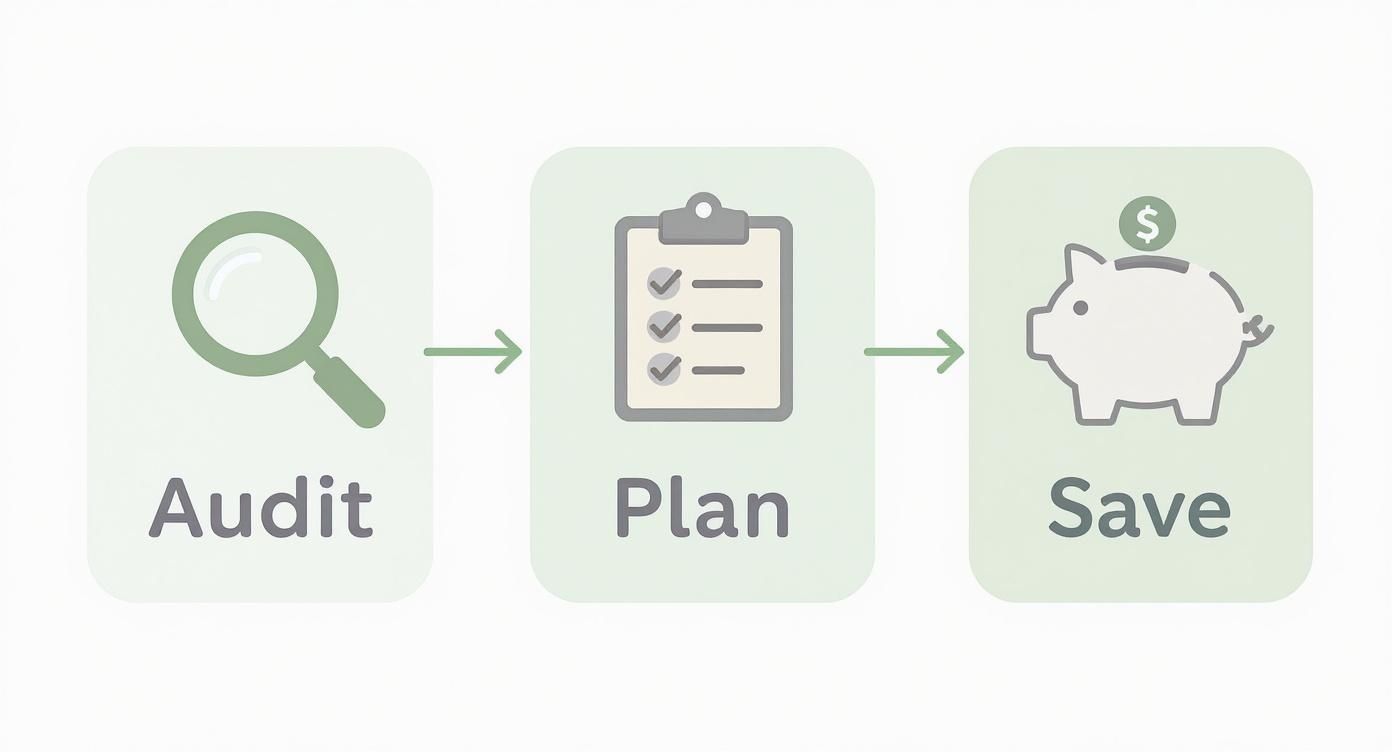

This simple process—Audit, Plan, and Save—is the bedrock of any good savings strategy.

As you can see, each step flows right into the next, creating a powerful cycle you can repeat to keep your money on track.

The Power of a Financial Audit

Before you can figure out where to save, you need a painfully honest picture of where your money is going right now. This isn't about feeling guilty over past purchases; it’s just a fact-finding mission. A proper audit means tracking every single penny for a full month.

You’ll probably be shocked by what you find. It’s often the small, almost invisible costs that do the most damage—that daily coffee, a handful of streaming services you barely use, or those free trials that quietly turned into paid subscriptions. They all add up.

A financial audit isn't about restriction; it's about awareness. Knowing where your money goes is the first and most critical step toward telling it where to go in the future.

Building Your Realistic Plan

Once your audit has exposed your spending habits, it’s time to build a realistic spending plan, or what most people call a budget. This isn't a financial straitjacket designed to make you miserable. It's a tool to help you line up your spending with what you actually earn and what you want to achieve.

Start by covering your essentials: housing, utilities, transport, and other core bills. After that, you can assign money to savings, paying down debt, and whatever is left for discretionary spending. The key is to create a framework that genuinely works for your life, not some idealised version of it. That’s the only way you’ll stick to it. We'll get into specific methods, like the popular 50/30/20 rule, a bit later.

Automating Your Success

This last part is where the magic happens. The single most effective way to guarantee you save money is to make it automatic. If you wait until the end of the month to see what’s “left over,” I can almost guarantee there will be nothing left. That’s just how it works, especially when money is tight.

The solution is simple: set up an automatic transfer from your main account to a separate savings account. Schedule it for the day after you get paid. Even if you start small, with just £10 or £20 per week, you’re building an incredibly powerful habit. This is the classic "pay yourself first" strategy, and it works because it puts your future self first, before the daily temptations can chip it all away.

A Realistic Budgeting Blueprint That Works

Forget those complicated spreadsheets and financial jargon. When you're figuring out how to save money on a tight budget, the last thing you need is a system that feels like a full-time job. The real goal is clarity, not complexity.

That’s why a simple, battle-tested framework is often the most effective.

This is where the 50/30/20 rule shines. It’s a straightforward way to budget that splits your after-tax income into three simple buckets. It gives every dollar a purpose without forcing you to track every single penny. This structure helps you prioritize what matters—savings and debt—while still leaving room to actually live your life.

Before we dive in, a quick note: The information here is for educational purposes to help you get started. It isn't professional financial advice. If you need guidance specific to your situation, I strongly recommend chatting with a qualified financial adviser.

Understanding the 50% for Needs

The biggest chunk of your income, 50%, goes toward your absolute essentials. These are the non-negotiable bills you have to pay to live safely and keep your job. Think of this as the foundation of your financial house.

This category covers things like:

- Housing: Your rent or mortgage payment.

- Utilities: Electricity, gas, water, and your basic internet connection.

- Transportation: Car payments, insurance, fuel, or public transport passes to get to work.

- Essential Bills: Core household costs required to function.

Getting honest about what’s a "need" versus a "want" is the most critical part here. A basic internet plan for work? That's a need. Upgrading to the fastest fibre-optic package for gaming? That slides over into the "wants" category.

Allocating 30% for Wants

Next up, 30% of your income is for your wants. This is the fun stuff—the discretionary spending that makes life more enjoyable but isn't strictly necessary for survival. This bucket brings flexibility and joy to your budget.

Spending here might look like:

- Entertainment: Streaming services, movie tickets, or going to a concert.

- Hobbies: Your gym membership, art supplies, or sports gear.

- Dining Out: Restaurant meals, grabbing coffee, or drinks with friends.

- Shopping: New clothes or gadgets that aren't essential replacements.

When money gets tight, this is usually the first area people look to trim. Tracking your spending here can be a real eye-opener, often revealing some surprisingly easy ways to save. For more ideas on this, check out our guide on the best money-saving tips.

Prioritizing 20% for Savings and Debt

Finally, a crucial 20% of your income is earmarked for your financial future. This bucket is your ticket to financial freedom, focused on building a safety net, wiping out debt, and eventually, building wealth.

This 20% isn't just leftover cash; it's a proactive investment in your future self. The simple act of "paying yourself first"—allocating this portion before you spend on wants—is a fundamental mindset shift that will accelerate your progress.

This money should be aimed at high-impact goals like building an emergency fund, aggressively paying down high-interest credit cards, or contributing to retirement accounts. The 50/30/20 rule is so widely recommended because it forces you to make savings a priority without demanding you give up your entire lifestyle.

To see how this works in the real world, let's look at an example.

Sample 50/30/20 Budget on a $2,500 Monthly Income

| Category | Percentage | Monthly Allocation | Example Expenses |

|---|---|---|---|

| Needs | 50% | $1,250 | Rent/Mortgage ($900), Utilities ($150), Groceries ($200) |

| Wants | 30% | $750 | Dining Out ($150), Subscriptions ($50), Shopping ($100), Hobbies ($50) |

| Savings & Debt | 20% | $500 | Emergency Fund ($200), Credit Card Debt ($200), Retirement Savings ($100) |

This table shows how a clear framework gives every dollar a job, making it much easier to see where your money should be going.

To make sticking to your plan even easier, you can use technology. Budgeting apps like YNAB (You Need A Budget) or Mint can sync with your bank accounts and automatically categorize your spending. It takes the tedious manual work out of the equation and gives you a real-time picture of your finances, helping you stay on track with your 50/30/20 plan without the headache.

How to Cut Your Spending Strategically

Once you have a budget mapped out, the real work begins: finding smart ways to lower your expenses without feeling like you're giving everything up. The key to saving money isn't about total deprivation. It’s about making high-impact cuts that actually create breathing room in your finances. We're going to focus on those sneaky, recurring costs that quietly drain your account month after month.

We'll hit three areas where a little bit of effort pays off big time, and keeps paying off. By auditing your subscriptions, negotiating your regular bills, and making small energy-saving tweaks, you can free up a surprising amount of cash. These aren't just one-time fixes; they're sustainable habits that put money back in your pocket every single month.

Conduct a Ruthless Subscription Audit

It’s just too easy these days. A free trial here, a one-click sign-up there, and before you know it, you’ve got a long list of forgotten monthly charges chipping away at your bank balance. That £9.99 for a streaming service you haven't watched in months or the £15 for an app you forgot you even had? It adds up fast.

Your first line of defense is a full-scale subscription audit. Pull up your bank and credit card statements for the last three to six months and highlight every single recurring payment. I guarantee you’ll find a few surprises.

If you want a shortcut, apps like Rocket Money or Trim can do the heavy lifting. You connect your accounts, and they automatically sniff out all your recurring payments, making it incredibly easy to cancel the ones you no longer need with just a tap.

The goal here is simple: only pay for services that are genuinely adding value to your life right now. If you haven't used it in the last 30 days, it’s on the chopping block. You can always sign up again later if you truly miss it.

Master the Art of Bill Negotiation

So many people just assume their monthly bills for things like internet, mobile phones, or insurance are set in stone. That's almost never true. Most providers have better deals and promotional rates available, but they aren't going to offer them unless you ask. One phone call can literally save you hundreds over the course of a year.

Before you dial, do a little homework. Hop online and see what their competitors are offering new customers for a similar service. This single piece of information is your most powerful negotiating tool.

Here’s a simple script to get you started:

- "Hello, my name is [Your Name] and I've been a loyal customer for [Number] years. I'm reviewing my budget and noticed my bill has gone up. I saw that [Competitor's Name] is offering a similar plan for £[Amount]. I’d really prefer to stay with you, so I was hoping you could help me find a more competitive rate."

Be polite, but be firm. If the first person you speak to says they can't help, just ask to be transferred to the customer retention department. It’s their entire job to keep you from leaving, which means they have the authority to offer the best discounts. This one move can easily shave £10, £20, or even more off your monthly outgoings.

Implement Smart Energy Efficiency Tweaks

Your utility bills are another goldmine for potential savings. You don't need to install solar panels to see a difference (though that's great if you can!). There are plenty of small, no-cost adjustments you can make today that will lower your energy use and your bills.

Start with the thermostat. Just turning it down by one degree can slash your heating bill by up to 10%. If you can, investing in a smart thermostat is a game-changer. It learns your routine and adjusts the temperature automatically, saving you money while you're asleep or out of the house.

Next, take a hard look at your energy tariff. Millions of people are on standard variable tariffs, which are usually the most expensive. Use a price comparison website to see if you can switch to a cheaper fixed-rate deal. The process is surprisingly simple and can save you hundreds of pounds a year. Some providers even offer cheaper electricity during off-peak hours, so you could save by running the washing machine or dishwasher overnight.

These financial adjustments are key to achieving financial freedom and reducing money worries. For more ideas, check out our guide on building an inexpensive healthy grocery list.

Building Your Financial Safety Net

https://www.youtube.com/embed/pEFWgW3UgfI

When you’re trying to save money on a razor-thin budget, the whole idea of an "emergency fund" can feel completely out of reach. But I'll be blunt: it's the single most important tool you have. It’s the wall that stands between an unexpected car repair and a devastating spiral into high-interest credit card debt.

This isn't a luxury item. It’s a non-negotiable part of getting your financial feet under you. The peace of mind that comes from knowing a surprise expense won't wreck your life is priceless.

Start Small, but Start Now

The advice to save three to six months of expenses is solid, but it can also be paralyzing. When you’re just starting, that number feels like a mountain. So, let's forget about it for a minute.

Your first mission is to hit a much more manageable target: $500.

Why $500? Because it’s enough to handle a lot of life’s annoying little emergencies—a busted appliance, a trip to the urgent care clinic, a last-minute flight for a family issue.

Achieving this mini-goal does two powerful things for you:

- It provides immediate breathing room: That $500 can solve a surprising number of problems without forcing you to pull out a credit card.

- It builds momentum: Hitting that first target proves to yourself that you can save. It gives you a huge psychological boost to keep going.

Once you have that initial fund secured, then you can start aiming for the bigger prize of three to six months' worth of essential living costs.

Put Your Savings on Autopilot

This is the secret weapon for anyone who struggles to save. You have to make it automatic. The "pay yourself first" strategy is a classic for a reason—it flat-out works.

Go into your banking app right now and set up a recurring transfer from your checking to a separate savings account. Schedule it for the day after you get paid. Even if you can only spare $10 or $20 a week, do it. The habit you're building is far more important than the dollar amount in the beginning. Those small, consistent deposits really do add up over time.

An emergency fund's true value isn't just the money. It's the options it gives you. It replaces panic with a plan and lets you handle life's curveballs with confidence instead of fear.

Keep It Separate and Accessible

For this to work, your emergency fund needs to live somewhere that's out of sight but not out of reach. That might sound contradictory, but it’s actually pretty simple.

Open a high-yield savings account (HYSA), preferably at a different bank than your main checking account. This separation creates just enough friction to stop you from dipping into it for a non-emergency, like a weekend sale.

But because it’s a savings account, you can still get the money within a day or two when a real crisis hits. This strategy protects your cash from you, while an HYSA lets it earn a bit more interest than it would in a regular account. For a deeper dive, you can learn more about how to build an emergency fund in our complete guide.

Recent numbers really drive this point home. While about 63% of Americans feel they could handle a $400 emergency, that leaves a huge number of people on shaky ground. And consider this: of those who recently used their emergency funds, 26% had to pull out between $1,000 and $2,499, which shows how fast things can escalate. You can find more of these emergency savings trends on Bankrate.com. A dedicated fund is what keeps these situations from turning into financial disasters.

Practical Ways to Boost Your Income

Cutting costs is absolutely essential, but let's be honest—you can only trim so much fat from your budget. At some point, the most powerful move you can make is to bring more money in the door. Boosting your income, even by a little, completely changes the game when you're saving on a tight budget. It's the other side of the financial coin, giving you the fuel to actually get ahead.

Before we dive in, a quick heads-up: The ideas here are for general guidance and educational purposes. My goal is to share practical tips that have worked for many, but this isn't professional financial advice tailored to you. If you need specific guidance for your situation, I strongly recommend chatting with a qualified financial adviser.

Now, this isn't about finding a second full-time job. Forget that. We're focusing on realistic, low-cost ideas you can squeeze into an already packed schedule. The aim is to generate an extra couple hundred pounds a month. That kind of cash can be a total game-changer for building your emergency fund or knocking out debt.

Put Your Existing Skills to Work

Chances are, you already have skills people will happily pay for. You just need to know where to find them. Thanks to the boom in freelance platforms, it's never been easier to connect with clients, even if you don't have a huge professional network.

Marketplaces like Upwork and Fiverr are overflowing with opportunities for all sorts of talents:

- Good with details? Offer your services as a virtual assistant. People pay good money for help with data entry, scheduling appointments, and managing chaotic inboxes.

- Got a creative spark? If you know your way around writing, graphic design, or social media, small businesses are always looking for help with their marketing.

- Tech-savvy? Skills in web development or even just being a whiz with spreadsheets are always in high demand.

The trick is to start small. Don't get overwhelmed. Just create a simple profile highlighting what you're good at, set a competitive rate to get your first few gigs, and then focus on knocking it out of the park to earn great reviews.

Tap into the Flexible Gig Economy

If your schedule is unpredictable, the gig economy can be a lifesaver. It’s built for earning money on your own terms. These jobs are perfect for fitting in around your main job or family duties because you can literally log on and off whenever you have a spare hour.

Delivery services are one of the easiest ways to get started. Companies are constantly looking for drivers to deliver everything from takeaway to parcels. The barrier to entry is low—you typically just need a reliable vehicle (a car, scooter, or even a bike), a smartphone, and to pass a background check. It's a straightforward way to turn a free evening or a quiet weekend into cash.

Boosting your income isn't just about the money; it's about reclaiming a sense of control. Earning extra cash, no matter the amount, reinforces a proactive mindset and directly counters the feeling of being trapped by a tight budget.

Turn Your Hobbies into Cash

This one can be the most rewarding. Turning something you genuinely love doing into a little side business is an incredible way to boost your income. Platforms like Etsy have opened up a global market for anyone making handmade goods or creating unique items.

Think about what you already enjoy doing in your downtime.

- Do you make cool jewellery?

- Are you a talented painter or digital artist?

- Do you have a knack for creating personalized gifts?

Startup costs can be next to nothing if you already have the supplies. Just list a few of your best pieces and spend some time taking really good photos—it makes a huge difference. As you make a few sales, you can reinvest that money back into your craft. This approach doesn’t just add to your bank account; it transforms a pastime into a real asset that helps you reach your financial goals.

Planning for Your Financial Future

Once you’ve got a handle on your day-to-day spending and have a small safety net tucked away, your focus can start to shift. You can move beyond just getting by and start thinking about long-term financial freedom. This is the exciting part—where you begin making your money work for you.

The two most powerful ways to do this? Strategically knocking out debt and starting to invest, even if you’re starting small.

A quick note: The goal of this guide is to share practical tips and insights that have worked for many people. However, this is for educational purposes and isn't professional financial advice. Everyone's situation is unique, so if you need advice tailored specifically to you, it's always best to chat with a qualified financial advisor.

Choosing Your Debt Repayment Strategy

Staring at a pile of high-interest debt can be overwhelming. It feels like a weight on your shoulders. The good news is there are proven battle plans to help you tackle it head-on. The two most popular are the debt avalanche and the debt snowball.

-

The Debt Avalanche: This one is all about logic. You make the minimum payments on all your debts, but you throw every extra dollar you have at the one with the highest interest rate. Mathematically, this is the quickest and cheapest way to get out of debt because you’re saving the most on interest payments.

-

The Debt Snowball: This strategy is more about psychology and momentum. You still make minimum payments on everything, but you focus all your extra cash on your smallest debt first, regardless of the interest rate. Once that’s gone, you take the money you were paying on it and roll it into the next-smallest debt. It creates a "snowball" effect that feels incredibly motivating.

So, which one is better? Honestly, the best method is the one you’ll actually stick with. The avalanche is technically more efficient, but don't underestimate the power of those quick wins from the snowball method to keep you fired up.

Demystifying Long-Term Investing

Investing can sound intimidating, like it’s something reserved for people with fancy suits and big stock portfolios. But it’s not. It’s simply the most reliable way for everyday people to build real wealth over time, and you don’t need a pile of cash to get started.

The real secret is consistency and a little something called compound interest.

This is where things get powerful. Compound interest is basically your investment earnings starting to generate their own earnings. It's a slow burn at first, but over decades, it creates an incredible snowball effect that can turn small, regular contributions into a serious nest egg.

For anyone learning to save on a tight budget, starting to invest is a huge mindset shift. You're no longer just saving for a rainy day; you're actively building the foundation for your financial independence years down the road.

A great, straightforward way to start is with broad-market Exchange-Traded Funds (ETFs). Think of an ETF as a basket that holds tiny pieces of hundreds or even thousands of different stocks. Buying into one gives you instant diversification, which is much less risky than trying to pick individual winning stocks.

Even with costs going up, there are positive signs. Recent data shows that 55% of U.S. adults have now saved enough to cover three months of expenses. You can dig into more of the numbers in these 2025 wealth statistics from The Economic Times. By setting up small, automatic investments into an ETF, you're putting that compounding magic to work for your future self.

Frequently Asked Questions

When you're trying to get a handle on your money, especially on a tight budget, questions are bound to come up. It's completely normal. Here are some straightforward answers to the things people ask most often, designed to keep you on track and feeling confident.

What Is the Fastest Way to Save $1,000?

Hitting a $1,000 savings goal fast requires a full-court press. You need to attack it from two angles at once: slash your spending to the bone and find a way to bring in extra cash, fast.

First, try a 30-day "spending freeze" on anything that isn't an absolute necessity. That means putting a pause on restaurant meals, new clothes, and any subscriptions you can live without for a month. It’s tough, but it’s a short-term sprint with a big payoff.

At the same time, you'll want to find a side hustle you can jump into immediately.

- Weekend Gig Work: Driving for a rideshare service or doing food delivery for a couple of full weekends can bring in a surprising amount of cash.

- Sell Your Stuff: We all have things lying around. Go through your home and list valuable items you don't use anymore—think old phones, furniture, or brand-name clothing—on an online marketplace.

- Quick Freelance Projects: If you have a marketable skill, hop on a platform like Fiverr and knock out a few small projects.

By combining an aggressive savings push with a quick income boost, you can realistically hit that $1,000 goal in just a few weeks. It’s a powerful way to build a starter emergency fund.

Is the 50/30/20 Rule Realistic on a Low Income?

Think of the 50/30/20 rule as a helpful starting point, not a hard-and-fast rule you have to live by. When you’re on a really tight income, the reality is that your "Needs"—like rent, utilities, and other bills—might eat up way more than 50% of your paycheck. That can leave very little room for "Wants" or "Savings."

The magic of the 50/30/20 rule isn't the specific numbers. It's the habit of thinking in categories: what you need to live, what you want for fun, and what you're putting aside for your future. That mental shift is the most important part of budgeting.

So, if the classic percentages don't work, change them. Maybe your budget looks more like 70/10/20 or 65/15/20. The most important thing is to fiercely protect that last number—the 20% for savings and debt—as much as you possibly can, even if it means the "Wants" category has to be tiny for a while.

How Can I Stay Motivated When Progress Feels Slow?

It’s completely understandable to get discouraged when you look at your savings account and see it growing by only small amounts. The trick to staying in the game is celebrating the small wins and finding ways to see your progress.

- Track Your Net Worth: This is a fantastic motivator. Even if your net worth only climbs by $50 one month, watching that number consistently go up is proof that you're moving in the right direction.

- Get Visual: Don't underestimate the power of a visual aid. Print out a savings thermometer or a chart to track paying off a credit card. Coloring it in as you hit new milestones feels incredibly satisfying.

- Reward Yourself (for free!): When you pay off a small debt or hit your first $100 savings goal, celebrate! Plan a relaxing night in with a movie you love or spend an afternoon at a park. Acknowledging your hard work keeps you going.

Just remember that building a solid financial foundation is a marathon, not a sprint. Every single dollar you save is a win.

At Collapsed Wallet, our whole mission is to give you clear, practical advice to help you become the boss of your money. We break down complicated financial ideas into simple, actionable steps you can use today to build a better financial future. Find out more at https://collapsedwallet.com.