Table of Contents

- Why Expense Tracking Is Your First Step to Financial Control

- Finding the Right Expense Tracking Method for You

- Building Your Personal Expense Tracking System

- Using Automation to Make Tracking Effortless

- Turning Your Spending Data into Financial Decisions

- Making It Stick: How to Stay Consistent and Sidestep Common Hurdles

- Got Questions About Tracking Your Expenses?

This blog post may contain affiliate links. As an Amazon Associate I earn from qualifying purchases.

Learning how to track your expenses is pretty straightforward: pick a method you'll stick with, set up some spending categories that make sense for your life, and make a habit of checking in on your numbers. This one habit can completely change your financial picture. It pulls back the curtain on where your money is actually going, giving you the power to make smarter decisions and start hitting your goals.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Why Expense Tracking Is Your First Step to Financial Control

Getting a grip on your finances can feel like a huge, intimidating project. The good news? It all starts with one simple, powerful action: understanding where your money goes. Think of expense tracking as the foundation of your entire financial house. It’s not about restricting yourself—it’s about getting an honest look at your spending habits to pave your way to financial freedom.

Without that clarity, trying to make real financial progress is like driving in the dark with no headlights. You might have big goals, like paying down your mortgage faster or finally dipping your toes into investing, but you won't have a clear roadmap to get there.

Gaining Clarity in a Complex World

We live in an age of invisible money. A quick tap of a card, a click on a website, and poof—the money's gone. This incredible convenience has a downside: it completely disconnects us from the impact of our small, everyday purchases. A coffee here, a new subscription there… it all adds up, silently draining your account before you even realize it.

Tracking your expenses forces a pause. It shines a light on that hidden spending and makes you mindful of every pound that leaves your account. It reconnects you to your financial reality, and that connection is where real control and the journey to escaping financial worries begins.

This isn’t just a personal finance trend, either. The entire world is moving toward instant financial insight. The global expense management market is on track to hit around $17 billion by 2032, and it's estimated that 75% of businesses will be using mobile apps for this by 2025. It just goes to show how powerful having real-time data at your fingertips can be.

From Awareness to Actionable Insight

Just knowing where your money goes is step one. The real magic happens when you start using that information to make deliberate choices. When you track your spending, you’re basically collecting data on your own financial behaviour.

By documenting every transaction, you move from passively spending to actively managing your resources. This simple habit is the difference between letting your money control you and you controlling your money.

This data helps you spot patterns you never would have noticed otherwise. You might be shocked to see how much you’re spending on takeaways or discover a few subscriptions you completely forgot you were paying for. Finding these "spending leaks" is the first step to plugging them and putting that cash toward things that help you achieve financial freedom.

Ultimately, tracking isn't about guilt or judgment. It's about empowerment. It’s a crucial piece of building the money management skills that will serve you for the rest of your life. With this knowledge, you can build a budget that actually works, set goals you can actually reach, and create a more secure financial future, one transaction at a time.

Finding the Right Expense Tracking Method for You

Let’s be honest: the best way to track your expenses is the one you’ll actually stick with. There's no magic bullet here. Choosing a method is a personal decision, and what works for a spreadsheet whiz might feel like a chore to someone who prefers pen and paper. The goal is to find a system that fits so naturally into your life that it becomes a simple, empowering habit.

The aim of our blog is to provide valuable insights and practical tips to help readers manage their money more effectively. However, the information shared here is for general guidance and educational purposes only. It should not be regarded as professional financial advice. Any actions taken based on our content are entirely the responsibility of the reader, and we accept no liability for the outcomes of those actions. If you require financial advice tailored to your personal circumstances, we strongly recommend seeking assistance from a qualified financial adviser.

Alright, let's look at the most common ways people get a handle on their spending.

The Classic Pen and Paper Method

You might think it’s old-school, but never underestimate the power of a simple notebook. There’s something about physically writing down every single purchase that makes you more mindful of your spending. It forces you to pause and acknowledge where your money is going in a way that tapping a card just can't.

This method is all about discipline, but it offers total simplicity and privacy—no apps, no data sharing. It’s perfect if you want to unplug and focus on the core habit. Just keep a small notebook in your bag or use a notes app on your phone to jot down purchases as they happen. Later, you can transfer them to your main ledger at home.

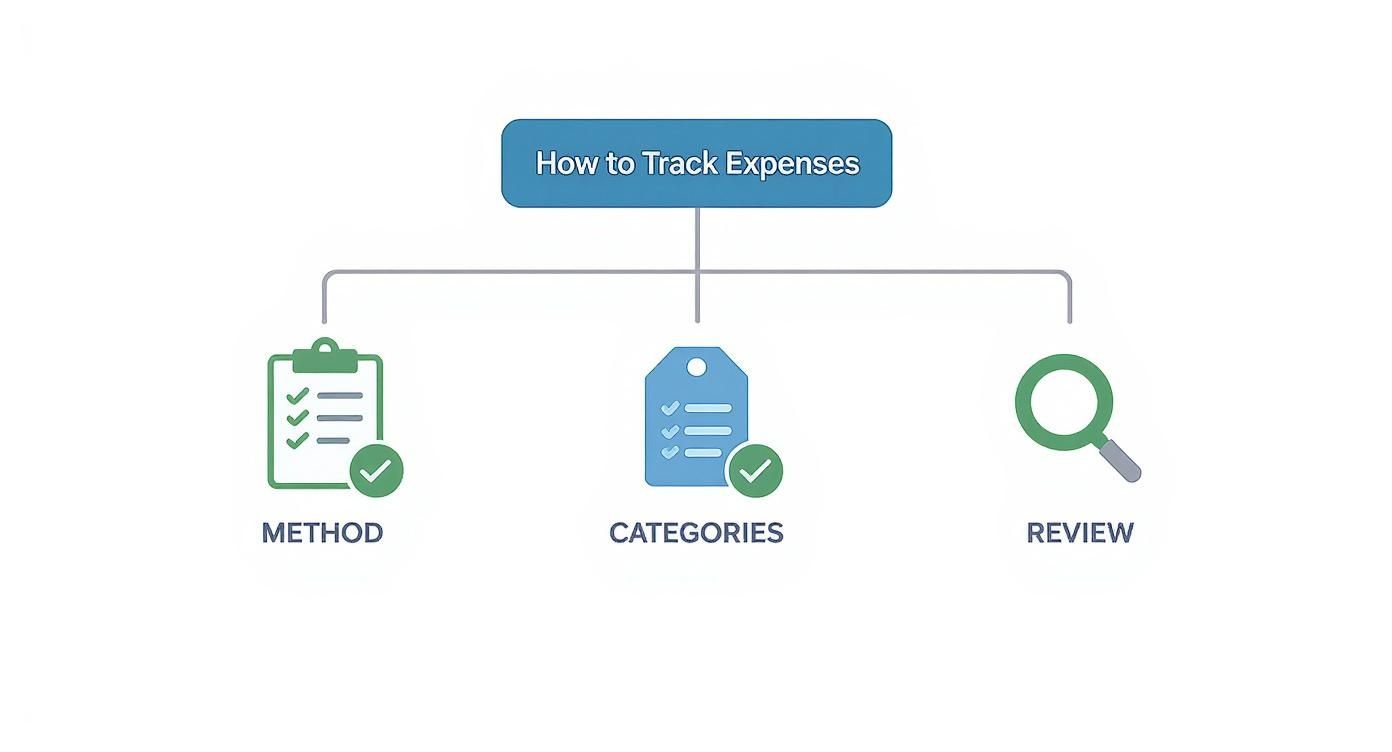

This infographic breaks down the fundamental steps, no matter which tool you end up choosing.

As you can see, the process is always the same: pick your method, sort your spending into categories, and make time to review the data.

The Flexible Digital Spreadsheet

If you're comfortable with a keyboard and want complete control, a spreadsheet is your best friend. Tools like Google Sheets or Microsoft Excel offer unlimited customization. You get to build your tracking system from the ground up, tailored exactly to your financial life.

You can create your own categories, build charts to see your spending trends, and design reports that make sense to you. Most people start with a simple setup with columns for:

- Date: When the transaction happened.

- Item/Description: A quick note on what you bought and from where.

- Category: Which spending bucket it falls into (e.g., Groceries, Transport, Bills).

- Amount: How much it cost.

The real beauty of a spreadsheet is that it can grow with you. As you get more advanced, you can add columns to track things like the payment method or whether an expense was a 'need' versus a 'want'. It perfectly blends the intentionality of manual entry with the analytical power of software.

The secret to making spreadsheets work is consistency. Set aside five minutes every evening or a dedicated slot on Sunday to update everything. If you let it pile up, it quickly becomes an overwhelming task.

The Automated Power of Budgeting Apps

For anyone who values convenience above all else, modern budgeting apps are a total game-changer. Apps like YNAB (You Need A Budget), Mint, or Emma can securely link to your bank accounts and credit cards to automatically pull in your transactions. This single feature eliminates the manual data entry that causes so many people to give up.

These apps give you a real-time financial dashboard right on your phone. Many also include powerful features like:

- Spending Alerts: Get a notification when you're about to overspend in a category.

- Financial Goal Tracking: See visual progress bars for your big goals, like saving for a down payment.

- Investment Monitoring: Some apps can also connect to your investment accounts to give you a full picture of your net worth.

While some of the best apps have a subscription fee, many people find they save far more than they spend just by having a crystal-clear view of their finances. If you're looking for a high-tech, low-effort solution, an app is probably your best bet. It really comes down to whether you prefer hands-on control or automated convenience.

Building Your Personal Expense Tracking System

So, you’ve picked your tool—the notebook, spreadsheet, or app that feels right. Now comes the important part: building a system around it that actually works for your life. This isn't just about logging numbers. It's about creating a framework that gives you real, meaningful insights. A well-designed system turns tracking from a chore into your most powerful tool for getting ahead financially.

The secret is making it personal. A generic template might last a week, but a system you build around your own spending habits, goals, and lifestyle is one you’ll stick with for the long haul. Let's walk through how to set this up from scratch so it’s effective from day one.

The Art of Granular Spending Categories

This is the most critical part of the setup. Defining your spending categories is where you'll get the clearest picture of where your money is actually going. Just labelling a category as ‘Food’ or ‘Transport’ is a start, but it’s too vague to help you make smart changes.

You need to get specific. This granularity is the difference between knowing you spend money on food and realising you could save £100 a month just by cutting back on takeaways. This is how you turn vague data into actionable information that leads to financial freedom.

Think about it this way:

- Instead of "Food," try: Groceries, Restaurants, Takeaway/Delivery, and Coffee Shops.

- Instead of "Transport," use: Petrol, Public Transport, Ride-Sharing, and Car Maintenance.

- Instead of "Bills," break it down to: Rent/Mortgage, Electricity, Gas, Water, and Council Tax.

- Instead of "Entertainment," split it into: Subscriptions (Netflix, Spotify), Cinema, Pubs/Nights Out, and Hobbies.

This level of detail helps you pinpoint exactly where you might be overspending. It also aligns your tracking with the real-world decisions you make every day, making the whole process feel much more intuitive.

Setting Up a Simple Spreadsheet Tracker

If you’ve decided to go the digital spreadsheet route, the goal is to create a template that’s easy to update but powerful enough to give you a decent summary. You don't need to be a spreadsheet wizard with complex formulas to start. A basic structure with four essential columns is all it takes to get going.

Here’s a simple example of what this could look like in Google Sheets.

The structure above is clean and simple. It makes daily entries quick and painless while still capturing everything you need for a solid monthly review.

Once you get comfortable, you can start adding more columns. Think about tracking the 'Payment Method' (debit, credit, cash) or adding a 'Need/Want' column to get even deeper insights. The beauty of a spreadsheet is that it can grow with you.

Configuring Your Budgeting App for Success

Using a budgeting app? The initial setup is absolutely crucial for making it work for you. Most of the heavy lifting is automated, but spending just a few extra minutes personalising it will pay off big time.

First things first: securely connect your bank accounts and credit cards. This is the core feature that allows the app to automatically pull in your transactions, saving you from the tedious task of manual data entry.

Once your accounts are linked, jump straight into the categories. The app will have a default list, but you should immediately edit it to match the granular list you already created. Delete any categories that are irrelevant to you and create custom ones that reflect your life. This alignment is what makes the financial reports accurate and useful.

Finally, set up some initial alerts. Most good apps let you create notifications for things like:

- Large transactions: Get an alert for any purchase over a set amount, like £100.

- Low balance warnings: Receive a ping when your current account dips below a certain threshold.

- Category spending limits: Get a heads-up when you’re about to hit your monthly limit for 'Restaurants' or 'Shopping'.

This proactive approach is becoming standard everywhere. A recent report highlighted that 70% of finance teams now consider real-time expense visibility their top priority. Setting up these alerts on your personal finance app gives you that same professional-level insight, helping you control spending as it happens. You can dive deeper into these findings by reading the full expense trends report.

Using Automation to Make Tracking Effortless

Let's be honest: the biggest reason people give up on tracking their expenses is because it feels like a chore. The secret to sticking with it is to make the whole process as painless as possible. While there's a certain satisfaction in manually writing everything down, technology can handle the grunt work for you. Automating the tedious parts frees you up to focus on what actually matters—understanding your spending habits, not just logging them.

This is where today’s financial tools really shine. When you set up a system that mostly runs on its own, tracking stops being a daily task and becomes a background process that quietly feeds you insights. The goal is to make it so seamless you barely notice it’s happening.

Let Bank Feeds Do the Heavy Lifting

The foundation of any good automated system is linking your bank accounts. When you connect your checking, savings, and credit card accounts to a budgeting app or a smart spreadsheet, you virtually eliminate manual data entry. This feature, usually called a bank feed, automatically imports every transaction into your system as it happens.

Forget about saving a pile of receipts to sort through later. Instead, you just open your app and see a list of your recent purchases already there, waiting for you. It's a total game-changer for consistency. It catches everything, from your mortgage payment to that morning coffee you forgot about, ensuring nothing slips through the cracks.

Create Rules for Effortless Categorization

Once your transactions are flowing in, the next step is to teach your system where everything goes. Most apps are pretty smart and will try to guess the category for you, but you can make the process nearly perfect by setting up your own rules.

Think about all your regular payments. You can create a rule that says any charge from "Netflix" always gets filed under "Subscriptions," or a payment to "SoCal Edison" goes straight into "Utilities." It's a simple "if this, then that" command.

By setting up rules for your frequent and recurring expenses, you can automate up to 80% or more of your transaction categorization. This is the difference between spending hours a month sorting data and spending just a few minutes reviewing it.

You set the rule once, and it works for you forever. Your spending reports stay organized and accurate with almost no ongoing effort. This is exactly why so many people have finally been able to stick with budgeting.

The business world figured this out a while ago. Companies using AI for expense tracking save an average of $75 per report, and 87% of Chief Financial Officers are now investing in automation. For the rest of us, this just shows how much time and headache you can save by letting technology handle the details. You can read more about these expense management trends and see how powerful this approach is.

Digitize Receipts on the Go

So what about cash purchases, or those paper receipts you need to keep for a warranty? There's an automated solution for that, too. Many budgeting apps now have a built-in receipt scanner.

Instead of stuffing crinkled receipts into a pocket, you can just:

- Snap a photo of the receipt with your phone.

- The app uses Optical Character Recognition (OCR) to read the merchant, date, and total amount.

- It then creates a new transaction for you, attaching the photo as proof.

This makes tracking cash—which is often the hardest part—incredibly simple. It finally closes the loop between your digital and physical spending, giving you a truly complete financial picture.

Automating these small habits can lead to big wins. For more ideas, check out our guide on the best money saving tips. By putting these tools to work, you're building a system that serves you, not the other way around.

Turning Your Spending Data into Financial Decisions

So, you’ve been tracking your spending. That’s a huge first step, but it’s only half the battle. The real magic isn't in just collecting the data; it's in what you do with it.

Knowing you spent £400 on groceries is interesting, sure. But using that information to find savings and redirect that cash towards your goals? That’s how you actually build wealth. This is the moment your tracking habit transforms from a chore into a powerful strategy for financial freedom.

The key is turning that raw data into smart decisions, and it doesn't have to be complicated. Building a simple weekly or monthly financial review habit is all it takes. Seriously, even 15-20 minutes is enough to get incredible clarity and start making meaningful changes.

Your Monthly Financial Review

Think of this as a regular, judgment-free check-in with your money. Find a quiet time, grab your spreadsheet or open your budgeting app, and get ready to look at your spending with curiosity. This isn't about beating yourself up for overspending; it's about understanding your habits so you can guide them better next month.

As you look over your categorized spending, start by asking yourself a few simple questions:

- What surprised me the most? Maybe your takeaway spending was double what you thought, or a forgotten subscription popped back up.

- Where did I nail it? Acknowledge the categories you stuck to. Celebrating wins builds positive momentum.

- Where’s the biggest opportunity to improve? Pick just one or two categories where you could realistically trim back.

This simple Q&A turns a boring list of transactions into a story about your financial life. It reveals the patterns and habits that are either helping you or holding you back.

A Practical Example: Turning Data into Action

Let’s walk through a real-world scenario. Imagine Alex has been tracking their expenses for a full month. During their review, they see their "Work Lunches" category hit £150. The number is a total shock; Alex had no idea buying lunch every day added up so much.

This single data point is the catalyst for change. Alex realizes this is 'want' spending, not 'need' spending, and it’s getting in the way of their goal to start investing.

The crucial insight isn't just that £150 was spent on lunches. It's the realization that this money has a higher purpose if redirected. It's the difference between a temporary convenience and a long-term asset.

Armed with this new awareness, Alex decides to act. They commit to bringing lunch from home four days a week, a simple adjustment that instantly frees up roughly £120 per month.

Now, Alex has options. That extra cash could be used to:

- Overpay a loan, saving on interest costs over time.

- Boost an emergency fund in a high-interest savings account.

- Set up a recurring investment into a low-cost ETF to get compounding on their side.

This is the entire point of tracking your expenses. The data spotted a financial leak, and a quick review turned it into an actionable plan. For more ideas on finding similar savings, check out our detailed guide on how to cut expenses.

By consistently reviewing your spending and acting on what you find, you create a powerful feedback loop that will accelerate your journey toward financial security.

Making It Stick: How to Stay Consistent and Sidestep Common Hurdles

Starting a new financial habit is one thing, but making it last is where the real magic happens. That initial burst of motivation you feel when you first start tracking your expenses can wear off, and that's completely normal. The key is building a system that can outlast the excitement.

It’s easy to get derailed, and I’ve seen it happen countless times. People often give up not because tracking is hard, but because they fall into a few predictable traps. Knowing what these are ahead of time is your best defense.

Pitfall #1: The Perfectionism Trap

This is, hands down, the biggest reason people quit. You miss a receipt from a cash purchase, and suddenly you feel like the entire month's data is shot. That all-or-nothing thinking is the enemy of progress.

Let me be clear: The goal here is progress, not perfection.

If you forget to log a few lattes or a tip you left in cash, it's not a big deal. Your data doesn't have to be flawless to give you powerful insights. Honestly, having an 85% accurate picture of your spending is a million times better than having a 0% picture because you gave up trying to be perfect.

Your goal isn't to account for every single penny. It's to understand the big-picture trends in your spending habits. Forgive the small slip-ups and keep moving forward.

Pitfall #2: The Over-Categorization Quagmire

When you're just getting started, it's so tempting to create a million different categories for every little thing. "Morning Coffee," "Lunch with Coworkers," "Weekend Drinks," "Takeout"… I've been there. While that level of detail seems smart, it quickly turns into a nightmare.

Too much complexity creates decision fatigue. You'll find yourself agonizing over whether that movie ticket goes under "Entertainment," "Social," or "Date Night." When logging a simple purchase feels like a chore, you're much less likely to do it.

My advice? Start incredibly simple. You can get away with just a few broad categories at first:

- Fixed Costs: Things like your rent/mortgage, utilities, and subscriptions. The non-negotiables.

- Variable Needs: Groceries, gas, and transportation. The stuff you need, but the amount can change.

- Wants: Pretty much everything else—dining out, shopping, hobbies, you name it.

You can always break these down into more specific sub-categories later, once the habit of tracking is firmly in place. Start simple to build momentum, and you'll be far more likely to stick with it for the long haul.

Got Questions About Tracking Your Expenses?

Once you start digging into your spending, a few questions almost always pop up. Getting those sorted out is key to building a tracking habit that actually sticks and helps you take control of your money. Let's tackle some of the most common ones I hear.

How Long Should I Track My Spending Before I Make a Budget?

You'll want to track everything for at least one full month. That gives you a decent snapshot of your typical income and where your money goes day-to-day.

But honestly, three months is the gold standard. Why? Because a longer timeframe catches all those non-monthly expenses that can wreck a budget—things like annual subscriptions, quarterly utility bills, or that yearly car service. A three-month view gives you a much more realistic picture, which is exactly what you need to build a budget you won't give up on after a few weeks.

What’s the Best Way to Track Cash?

Ah, cash. It's the easiest money to spend and the hardest to track. The secret is simple but requires a little discipline: log it the moment you spend it. If you wait until the end of the day, you’ll inevitably forget that coffee or those snacks.

Here are a couple of practical ways to handle it:

- Your Phone is Your Best Friend: The second the cash leaves your hand, pull out your phone. Pop the transaction into your budgeting app or even just a basic notes app.

- The Receipt System: Pick a specific pocket in your wallet or purse just for cash receipts. At the end of the day, make it a five-minute habit to go through them and log each one in your app or spreadsheet.

This might feel tedious at first, but it stops those little cash purchases from becoming a huge "mystery" spending category that throws off your whole budget.

Remember, the goal isn't just to see where money went, but to understand your habits. Consistent tracking, even for small amounts, provides the clarity needed to make impactful changes.

Okay, I've Tracked My Spending… Now What?

This is where the magic happens. The first thing to do is look at what you’ve tracked and split it into two simple piles: 'needs' and 'wants'. Needs are the essentials like your rent or mortgage, utilities, and groceries. Wants are everything else—dining out, entertainment, hobbies, that daily latte.

Now, zoom in on your 'wants' category. Pinpoint the top one or two areas where you spent the most. Instead of trying to cut back on everything all at once (which is a recipe for failure), just pick one of those top areas to focus on. This small, targeted approach feels way more achievable and gives you a quick win, building the momentum you need to tackle bigger financial goals.

At Collapsed Wallet, our entire focus is on giving you clear, no-nonsense advice to help you master your money. To keep building your financial confidence, check out more of our resources at https://collapsedwallet.com.

22 thoughts on “How to Track Your Expenses for Financial Clarity”